Use of runner-up evidence in merger assessments

Share

What should be the role of runner-up evidence in bidding analysis when assessing mergers? The European Commission discussed this issue extensively in the GE/Alstom case, and various of its subsequent decisions have referred to this case. In this article, Segye Shin [1] reviews the approach taken in the case and derives lessons for future cases, explaining the relevance of runner-up evidence under different auction frameworks.

View the PDF version of this article.

The views expressed in this article are the views of the authors only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

Introduction

Quantitative evidence from historical tenders has been an important information source in several merger assessments by European competition authorities. Depending on the context, merging parties may have “bidding data” at their disposal, consisting of information on the tenders that they have participated in, the characteristics of the customer, the competitors that took part, and the outcomes of the tenders. Competition authorities have become used to working with bidding data from historical tenders, and certain types of analyses on such data have become standardised.[2]

When firms compete mainly through tenders, economic theories of auctions provide valuable insight on how competition in these types of markets should be assessed.[3] In one particular merger assessment by the European Commission, this link between economic theory and bidding data came to the fore: in GE/Alstom, [4] the Commission examined data submitted by the merging parties on the frequency with which the merging parties placed as winners and runners-up in historical tenders. The Commission’s decision in this case advanced the view that the relevance of this evidence depends on the exact economic model of auctions that best represents the form of competition in the market, such that runner-up evidence is relevant when analysing some types of tender, but less so when analysing others. The view has been influential. Several subsequent decisions cite GE/Alstom as a guide for their methodology relating to bidding data.[5]

This article sets out the Commission’s viewpoint with regards to runner-up evidence in GE/Alstom and explains why it should be re-examined. In principle, economic theory predicts that runner-up evidence is always relevant, regardless of the auction framework. In practice, the apparent influence of GE/Alstom on subsequent cases risks throwing away evidence that could otherwise show how closely merging parties compete in tenders.

Analysis of bidding data in merger assessments

In markets where competition takes the form of tenders for discrete large contracts (as opposed to serving an atomised set of small customers) it is common for suppliers to record information on the tenders that they have participated in. This can occur in many business-to-business (B2B) industries, for example, and may be aided by internal systems such as customer relationship management (CRM) tools. The types of data typically available on historical tenders have led to some standardised analyses that have been used in multiple previous merger assessments by the European Commission. Among these are:

- Participation analysis, i.e., analysis of how often the merging parties participate in tenders against each other; and

- Loss analysis, i.e., analysis of how often the merging parties lose to each other in tenders.

These analyses require data on the identity of competitors participating in each tender and the identity of the final winner of the tender. Merging parties are often able to provide data on at least their own participation in historical tenders, and the identity of the winner may also be reasonably well known based on the merging parties’ business intelligence.

The Commission’s approach to runner-up evidence in GE/Alstom

Richer data on tender outcomes may also be available in some instances, depending on the industry context as well as the way that firms capture data. During certain merger assessments, the merging parties have been able to provide data on the relative placements of the competitors involved in historical tenders. One example of this was GE/Alstom, where the merging parties produced evidence on which competitors placed as runners-up in historical tenders.[6]

The merging parties in this case submitted the following arguments to the Commission, based on their relative placements in historical tenders.

- The tenders in the industry were characterised by multiple rounds, including a “shortlist stage” and a “runner-up” stage. The latter in particular allows the merging parties to reliably identify which bidder among the losers was the runner-up bidder for each tender.

- The analysis of this runner-up data showed that when one of the merging parties was the winner of the tender, the other merging party was rarely the runner-up bidder.

The Commission’s decision included an extensive annex setting out an analysis of the bidding data and an assessment of the merging parties’ arguments. On the facts, the Commission disagreed with the merging parties’ views that the bidding data contained robust evidence of the identity of runners-up in historical tenders, which formed part of the Commission’s reasoning for dismissing the merging parties’ arguments.

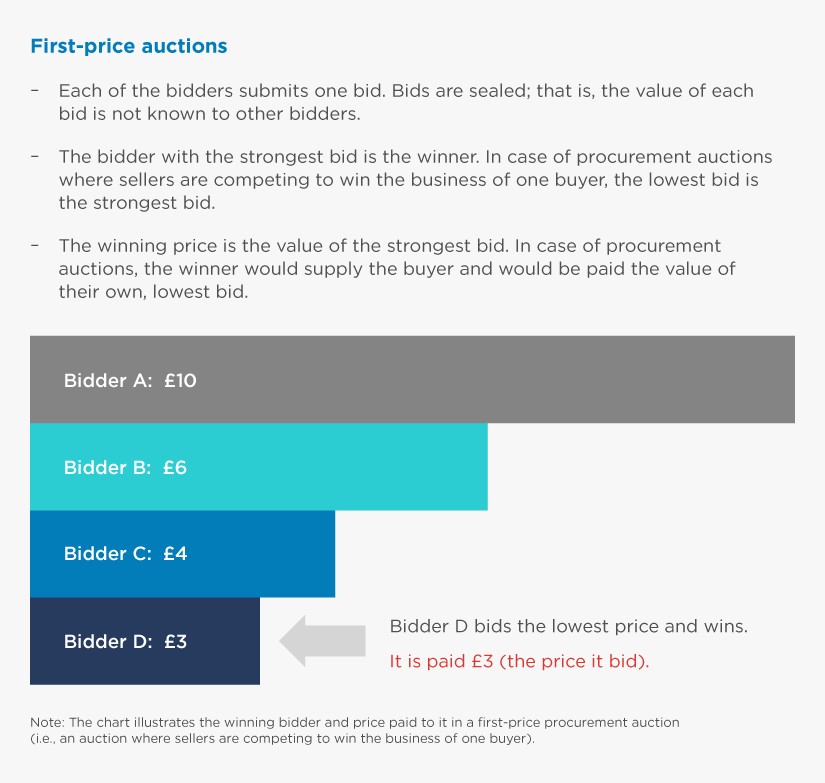

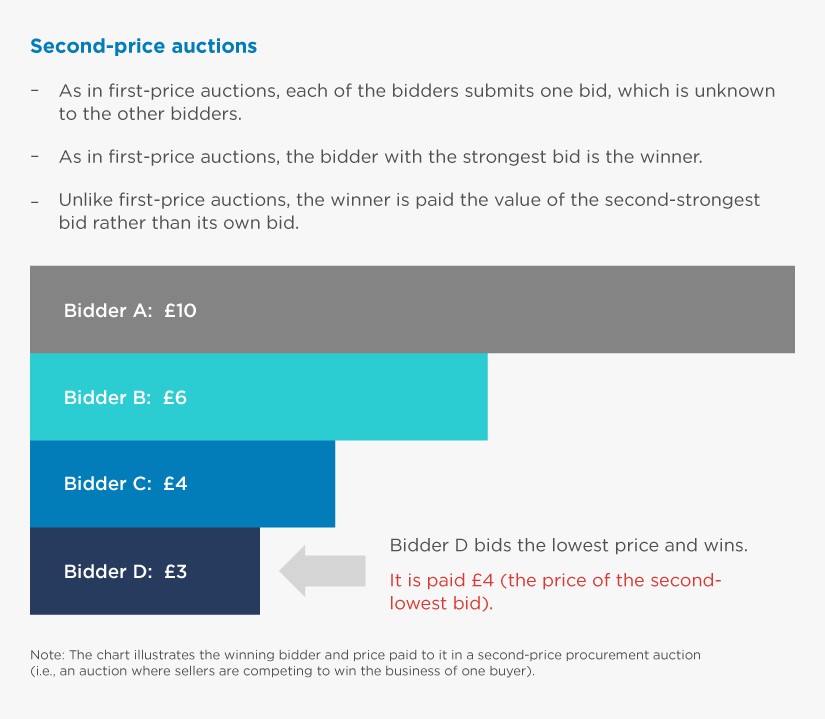

However, the Commission also wrote about the relevance of runner-up evidence. In particular, its decision considered – citing economic theory – that the relevance of runner-up evidence depended fundamentally on the exact form of tenders that prevailed in the market: specifically, whether the tender was a “first-price auction” (where the winning bidder receives the price that it bid – see Box 1 “First-price auctions” for details), or a “second-price auction” (where the winning bidder receives the price that the runner-up bid – see Box 2 “Second-price auctions” for details).

The decision suggests that runner-up evidence would be relevant in second-price auctions.

“In a second-price auction setting, a merger will affect the winning bid if it brings together the two firms that are best placed to serve a customer. […] No bidder other than the winner and the runner-up matter for the determination of the winning bid, and more generally for the outcome of the auction.”[7]

In contrast, the decision suggests that under first-price auctions, the identity of the runner-up in particular is not relevant compared to data on all other bidders also participating in the auction.

“The incentives to increase bids in a first-price auction following a horizontal merger are very similar to those at work in markets with differentiated products. The primary difference is that the diversion of sales between competing firms should be understood in terms of the expected sales (i.e. the probability of winning the tender) rather than actual sales.”[8]

“The effects of mergers in sealed bid-auctions with imperfect information are likely to affect a relatively broad class of buyers, rather than being targeted on customers for whom the merging parties are the two preferred bidders. This follows from the fact that bidding incentives will change for all tenders where the merging parties consider that the winning probability of one of the merging firms would be affected by the bid of the other merging firm (and vice versa). This includes also tenders in which the two merging firms are not the two best-placed firms…”[9]

“In practice, all bids where the merging parties would have met absent the merger […] are apt to be affected by merger effects.”[10]

Based on these views of first and second-price auctions, the decision appears to define a rule for whether runner-up evidence is relevant:

- if the relevant market is characterised by second-price auctions, then this evidence is relevant, potentially above any other quantitative evidence to be derived from the data.

- “First, focusing exclusively on runner-up data […] would be justified under a second-price auction environment [...]”[11]

- If the relevant market is characterised by first-price auctions (or any other auction framework), then such evidence holds less relevance and the Commission would disregard such evidence in favour of other analyses such as participation and loss analyses explained above.

- “[T]he Commission is not aware of auction models other than the second-price auction (or descending auction format) which would deliver the prediction that only the behaviours of the winner and of the runner-up bidder matter for the determination of the outcome of the auction, and that other bidders have no impact on the price formation process.”[12]

In fact, that approach is not entirely consistent with how economists think about auctions. Economic theory predicts that information on the identity of the runners-up in auctions should always be relevant, as it provides valuable evidence on the closeness of competition between the merging parties regardless of the exact auction format.

Why focusing exclusively on runner-up data is not justified under a second-price auction framework

Under a second-price auction, all bidders taking part in the auction submit a bid, the bidder with the strongest bid is chosen as the winner and the price paid is equal to the second strongest bid. According to a well-known result in auction theory, this auction structure incentivises all bidders to bid their true valuations, and this is not affected by either the number or the identity of the other participating bidders.

Based on this structure, focusing exclusively on the runner-up evidence appears to be justified at first glance. According to the bidding incentives explained above, removal of any of the bidders from the auction process does not affect the bidding strategies of the remaining bidders. Moreover, for a given set of bids submitted by bidders, the removal from the process of any bid other than the bids of the winner and the runner-up would not affect the auction outcome in terms of either the winner or the winning price. Therefore, if a given historical tender had been repeated without the participation of any bidder other than the two lowest bidders, the auction outcome would not be affected in any way.

However, it is problematic to conclude based on this line of reasoning that competitive constraints from all bidders other than the top two bidders in historical tenders can be ignored. Assessments of merger impacts should examine the impact of the merger on the factual and counterfactual scenarios in future tenders, not historical tenders that have already taken place. The historical tenders are of course important in empirically establishing the conditions of competition in the market, but the conceptual question asked by the competition authority should not be “what would the merger effect have been on past tenders that have already occurred”, but rather “what would be the merger effect on the tenders that will take place in the foreseeable future, for which past tenders act as a proxy and a source of evidence?” Focussing exclusively on the top two bidders in historical tenders amounts to an assumption that the bids and relative rankings of competitors in future tenders would perfectly mirror the outcomes of past tenders.

The risks of this line of reasoning can be illustrated with an example. Suppose that in a dataset of historical tenders in a market characterised by second-price auctions, a supplier which often participates in tenders is never observed to be one of the top two bidders. Focussing on runner-up evidence exclusively would lead one to conclude that such a supplier presents zero competitive constraints on other bidders, and that a merger involving that supplier would represent no change in competition in the market. This is in fact a possibility, but would only hold true if the supplier was at such a disadvantage compared to the rest of the bidders that it had no possibility of winning any tender in any circumstances. In reality, this is an unlikely scenario and it would be unclear how such bidders would exist in the market or why they would participate in any tenders. A merger assessment based on a broader view of the evidence would likely find that such suppliers present some, albeit weaker, competitive constraints on other suppliers, which is a more reasonable view of the evidence.

Similarly, when examining a dataset of historical tenders, one may find that the merging parties were never the two top-placed bidders. Again, it is possible that in tenders where one of the merging parties is the winner, the other merging party is at such a disadvantage that it presents zero competitive constraints on other bidders. However, a more natural interpretation of the fact that it is participating in the tender would be that it presents some, albeit weaker, competitive constraints on other suppliers.

It is important to note that this does not imply that runner-up evidence from historical tenders is irrelevant. On the contrary, robust findings of patterns for runners-up in historical tenders is valuable for the assessment of mergers because it provides evidence on the closeness of competition between different bidders. If, for example, the merging parties could provide credible evidence that they had seldom been the two top-placed bidders in the same historical tenders, this should lead to the conclusion that they are not each other’s closest competitors and therefore they are less likely to represent the most significant constraints on each other’s prices in future tenders. The clearer the finding on the two top-placed bidders, the more confident a competition authority can be that this analysis provides robust evidence on closeness of competition.

This is not a new idea, and parts of the GE/Alstom decision note this logic.

“Non-coordinated merger effects in second-price environments are therefore a function of the probability with which the two merging parties can be expected to be winner and runner-up in tenders. This probability is often approximated by looking at the frequency with which the merging parties were winner and runner-up in past tenders. However, the OFT (2007) correctly cautions against this approach, as it presupposes that one can be certain who the strongest two bidders are in advance of a given bidding process. In practice, a bidder participating in a descending auction will do so because it considers that it has a material chance of winning the tender (especially if participation costs are significant). Removing this bidder through a merger can therefore be expected to have some effect on the bid-taker, even if in past bids the bidder had not frequently been a runner-up to the other merging party (or vice versa).”[13]

Why runner-up data remains relevant under a first-price auction framework

Under a first-price auction, the winner of the auction is the bidder with the strongest bid and the price paid is equal to the value of the winning bid. Therefore, unlike second-price auctions, there is no direct relationship between the winning price and the value of any of the bids other than the winning bid.

In this setting, bidding up to one’s true valuation as in a second-price auction is an unwise strategy because winning based on such a bid would leave the bidder no better off than not participating in the tender at all. Economic theory instead predicts that each of the bidders in the auction would form their bids based on weighing up the rewards of winning the auction at a more favourable price against the risk of losing the auction to another bidder that undercuts them. This trade-off was also explained in the GE/Alstom decision.

“Under a sealed-bid format, the pricing incentives of competing firms closely resemble those at work in ordinary markets with differentiated products. If there is uncertainty on the required level of the winning bid, each firm will face a trade-off between the probability of winning the tender and the margin earned in case of winning the tender. A higher bid will reduce the probability of winning the tender but will increase the margin if the bid is successful. This tradeoff is equivalent to the standard tradeoff between quantity sold and price in an ordinary differentiated goods market, with the difference being that in the case of a tender it is the expected quantity sold (i.e. the probability of winning the auction) rather than actual quantity sold which enters the tradeoff. Each bidder therefore chooses its optimal bid in order to optimise the tradeoff between expected sales and price and thereby maximises its expected profits. Pricing incentives and the related incentives to exploit market power are therefore analogous to those at work in standard pricing of differentiated products.”[14]

This does not appear to leave any room for runner-up evidence to play a part in the assessment of merger effects, and the Commission notes that “[t]he effects of mergers in sealed bid-auctions with imperfect information are likely to affect a relatively broad class of buyers, rather than being targeted on customers for whom the merging parties are the two preferred bidders” and “[i]n practice, all bids where the merging parties would have met absent the merger (which can be proxied by bids where the parties have actually met in the recent past) are apt to be affected by merger effects.”[15]

However, evidence on runners-up is relevant in the assessment of first-price auctions, and the reason for this is similar to that discussed for second-price auctions above: robust evidence on runners-up in past tenders provides valuable evidence on the closeness of competition between different bidders.

To illustrate, suppose that the merging parties provide credible evidence that they had seldom been the two top-placed bidders in historical tenders. This should lead to the conclusion that they are not each other’s closest competitors, and that they will have little impact on the trade-off between price and winning probability faced by the other party in future tenders. As such, their respective market shares are overstating their degree of competitive constraints on each other.

In contrast, suppose that in all tenders that one of the merging parties wins, the other places second. This should lead to the conclusion that the merging parties represent the most important drivers of the trade-off between price and winning probability faced by the other party. Removal of the parties as a competitive constraint is likely to have a strong impact on these trade-offs in future tenders in favour of higher prices.

As suggested by the parallel between first-price auctions and ordinary differentiated markets, this is similar to how diversion ratios would be interpreted in any merger assessment of differentiated products. As noted by the Commission:

“The incentive to increase bids in a first-price auction following a horizontal merger are very similar to those at work in markets with differentiated products. The primary difference is that the diversion of sales between competing firms should be understood in terms of expected sales (i.e. the probability of winning the tender) rather than actual sales. […] The diversion ratio between Firm A and Firm B is therefore determined by the fraction of the reduction in Firm A’s winning probability that is captured by Firm B (and vice versa for the diversion ratio from Firm B to Firm A).”[16]

Under this interpretation, historical runner-up evidence is relevant for assessment of merger effects because it reveals which bidders would be best placed to capture the winning bidder’s reduction in the probability of winning the tender, should that bidder bid less aggressively in future tenders. Discarding the historical runner-up evidence and relying on other analyses such as participation and loss analyses means throwing away potentially valuable information that could shed light on the true competitive dynamics in the market.

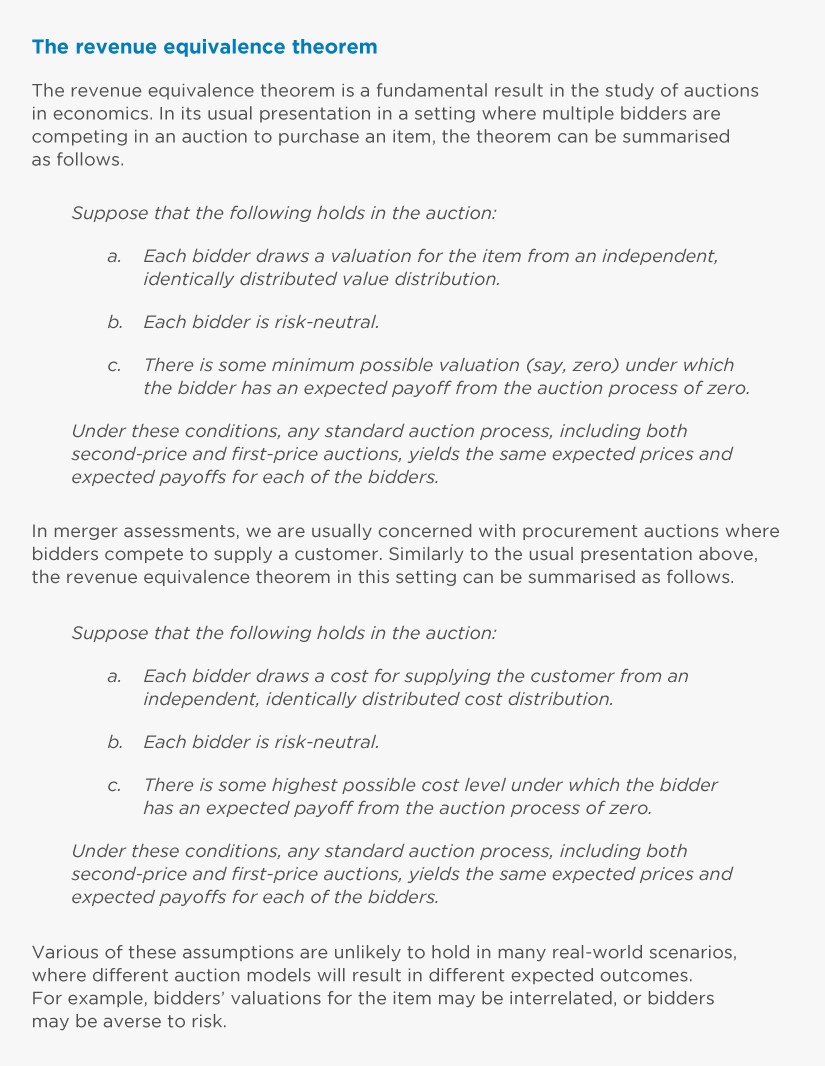

Revenue equivalence

Economic theories of auctions demonstrate that information on the identity of the runners-up provides valuable evidence on closeness of competition regardless of the exact auction format. The differences between first-price and second-price auction structures do not give rise to a fundamental change in the relevance of this type of evidence. This can be starkly demonstrated with the revenue equivalence theorem.

The revenue equivalence theorem is a fundamental result in economic theories of auctions which shows that under certain conditions on the bidders' underlying costs and their attitude to risk, both first-price and second-price auctions (and many other auction structures) yield the same expected auction outcomes – such that the expected auction price, and each bidder’s probability of winning, will be the same whichever specific structure is used. The exact structure for the auction, in other words, does not affect the expected outcomes if the underlying set of bidders and market conditions remain the same. Given these inputs into the auction process, each of the bidders strategises to make their bidding decisions in such a way that the differences between first-price and second-price auction structures are nullified, yielding the same auction outcomes across the two structures in expected terms.

The revenue equivalence theorem is a striking result, and it does depend on strict conditions that oversimplify the environments in which firms compete in real life. However, it serves to illustrate one of the key insights from economic theories of auctions, namely the commonalities between different forms of auctions such as first-price and second-price auctions. Under both of these structures, the set of bidders involved in the auction impose varying degrees of competitive constraints on each other, determined by their relative valuations and closeness of competition. Even when the more complicated environments that may apply in real life are considered, the importance and nature of those constraints remain.

Accordingly, one should be wary about linking the interpretation of evidence from historical tender outcomes to whether the tenders can be best characterised as first- or second-price auctions. When faced with runner-up evidence from historical auctions, for instance, the default position should be that such evidence provides a potentially useful view of the closeness of competition between competing bidders, independent of the assumed auction framework.

Conclusion

Economic theory can be a powerful tool to aid interpretation of data. However, it should be applied carefully, based not only on an examination of the economic literature but also the way that competition actually operates in the market under examination.

The convention emerging from GE/Alstom – that runner-up evidence does not hold much relevance under the first-price auction framework, but it should be the focus of the assessment when analysing tenders with a second-price auction framework – is not supported by economic theory. The insight that arises from economic models of first-price and second-price auctions is that all bidding data helps us understand the underlying competitive constraints that are common to different auction structures. In the either framework, evidence on how frequently two parties have been runners-up to each other is evidence on how closely they compete.

In GE/Alstom, the Commission also carried out an examination of the quality of the runner-up evidence submitted by the merging parties and found that the evidence was not credible. In the end, therefore, the Commission’s views relating to economic models of auctions may not have been the determinative factor in its dismissal of the runner-up evidence in that case. However, the rationale has influence. As historical tender data continues to be used by the Commission and other competition authorities as a source of quantitative evidence, however, a re-examination of that logic is valuable, in order to avoid conceptual errors that may sway other merger assessments in the future.

Read all articles from this edition of the Analysis

View the PDF version of this article

[1] Segye Shin is a Vice President at Compass Lexecon. The views expressed in this article are the views of the author only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

[2] Some recent examples of European Commission (“EC”) merger assessments that have examined bidding data include Case No. M.9585, Outotec/Metso (Minerals Business); Case No. M.9985, Gardaworld/G4S; Case No. M.10078, Cargotec/Konecranes.

[3] See for example Klemperer, P. (2007), “Bidding Markets”, Journal of Competition Law & Economics, Volume 3, Issue 1, pp. 1-47.

[4] Case No. M.7278, General Electric/Alstom (Thermal Power – Renewable Power & Grid Business) (“GE/Alstom”).

[5] For example, Case No. M.7555, Staples/Office Depot cites GE/Alstom when discussing the role of the runner-up bidder in determining auction outcomes in second-price auctions. Other EC decisions that cite GE/Alstom on points relating to bidding analysis include: Case No. M.8677, Siemens/Alstom; Case No. M.9076, Novelis/Aleris; Case No. M.9820, Danfoss/Eaton Hydraulics; Case No. M.9969, Veolia/Suez; Case No. M.10078, Cargotec/Konecranes.

[6] Case No. M.7278, General Electric/Alstom (Thermal Power – Renewable Power & Grid Business), Art. 8(2) EC decision dated 8 September 2015, Annex I (henceforth, “Case No. M.7278, GE/Alstom, EC decision, Annex I").

[7] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 28.

[8] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 15.

[9] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 16.

[10] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 16.

[11] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 147.

[12] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 149.

[13] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 29.

[14] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 13.

[15] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 16.

[16] Case No. M.7278, GE/Alstom, EC decision, Annex I, para. 15.

Related insights

-

The Analysis • 13 Jun 2023

The special merger regime for energy networks: lessons from the water sector

-

The Analysis • 13 Jun 2023

Data traffic and network infrastructure investment: the debate

{kind=link}

{kind=link}

{kind=link}