Data traffic and network infrastructure investment: the debate

Share

Telecommunications network operators, providers of online content, and regulators debate whether content providers should contribute to the costs of network infrastructure to promote efficient investment. In this article, Guillaume Duquesne, Cecilia Nardini, and Gabriele Corbetta [1] review the debate and policy options.

View the PDF version of this article.

The views expressed in this article are the views of the authors only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

Introduction

In its recent consultation on “The future of the electronic communications sector and its infrastructure”, [2] the European Commission (hereafter “EC”) identifies a potential “paradox between increasing volumes of data on the infrastructures and alleged decreasing returns and appetite to invest in network infrastructure”.[3]

The consultation follows claims by some European telecommunications network operators (hereafter “network operators”). They argue that while network usage is increasing, return on investment is decreasing. This reduces incentives to invest. If true, that could be a problem. If network operators underinvest, it harms both consumers that demand data and companies that rely on the network to supply content and services (hereafter “content providers”). But it shouldn’t be true, hence the “paradox”: if investing in network infrastructure creates value, someone should be willing to pay for it unless there is a market failure.

The issue is creating a contentious debate.

- On one side, several network operators have argued that content providers whose services stimulate internet traffic should contribute to infrastructure costs, to ensure sufficient investment. This is the so-called “Fair Share Proposal”. The proposal has some support from regulators across the Atlantic, such as Brendan Carr, commissioner at the Federal Communication Commission (“FCC”), the US telecommunications regulator.[4]

- One the other side, the Body of European Regulators for Electronic Communications (hereafter “BEREC”), the Europe-wide sectoral regulator, is sceptical. So are industry associations representing content providers and the Dutch government. They doubt there is underinvestment. And if there is, they doubt that allowing network operators to charge content providers would fill the gap.

In this article, we provide an overview of the debate and identify the key questions that the EC will have to address.

Do network operators underinvest in infrastructure?

The first key question is whether there is underinvestment, i.e., whether network operators will support the growing demand for data with sufficient investment in infrastructure. This is a factual question.

Growing demand for data

Data usage has grown and grown quickly. In 2022, consumers used 23% more data than the year before, continuing an annual growth rate in total internet traffic, on fixed and mobile networks. Internet traffic increased 3.2-fold from 2018 to 2021.[5]

In part, that reflects how our habits have changed after Covid: even after the end of the restrictions, for example, many of us work remotely to a greater extent.[6] But it also reflects underlying developments in telecommunications technology and the services it makes possible.

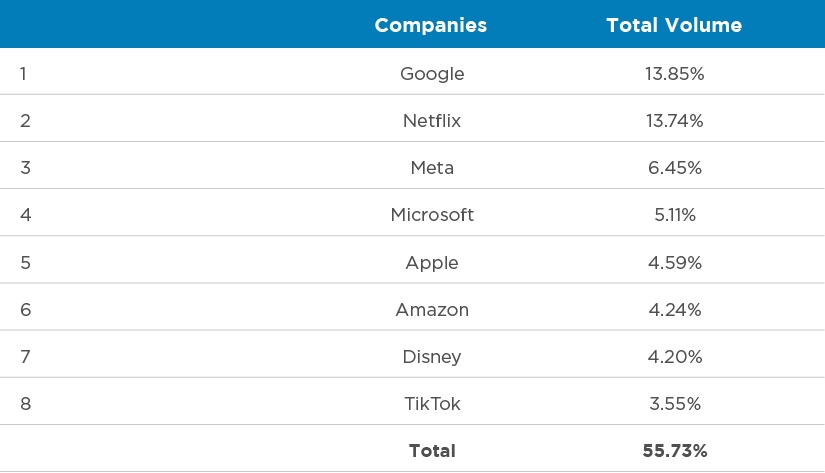

Video content now accounts for around two thirds of all internet traffic.[7] Relatively few content providers stimulate most of that demand for data. Eight companies account for more than half of all internet traffic, according to Sandvine, an app and network intelligence company. The leading content services are Netflix (accounting for 13.74% of traffic) and Google’s YouTube (which alone accounted for 10.51% of traffic).[8]

Table 1: The services of eight companies stimulated over 50% of all internet traffic in 2022

Source: Sandvine (2023), “2023 Global Internet Phenomena Report”, pp. 10-15.

Note: Due to data availability, “Disney” only relates to traffic related to its Disney+ service as reported by Sandvine.

Demand for data should continue to grow: governments pin their hopes for economic growth on new technology and broad access to it. For instance, the EC’s ambition is that, by 2030, 5G covers all populated areas in the EU by 2030 and all European households have access to a gigabit network.[9] New technology – whether 5G or gigabit broadband – is not simply about maintaining demand for the services currently on offer; it should enable new services and opportunities, for instance, in telehealth, online education, and possibly for products no one has considered yet. Ofcom’s medium growth forecast is for mobile data traffic in the UK to grow 40% on average per year to 2035.[10]

Investment in infrastructure

Network operators invest a lot in infrastructure.

In 2021, total telecom capital expenditure in Europe reached €56.3 billion.[11] That investment is expected to grow. Investment to increase capacity and performance so that the full potential of 5G is realised and to extend 5G coverage is estimated to require 2.4 times more capex over 2020 to 2027 than 2018 capex levels.[12] Achieving the EC’s full 5G coverage target by 2030 is estimated to require an additional €150 billion of investment.[13]

There is some debate about whether increasing demand really requires additional investment. For instance, BEREC and the Dutch government consider that higher traffic does not necessarily translate into higher costs for the network operators: up to a point, existing networks can accommodate higher capacity. BEREC believes that relatively small investments are needed to handle increased IP traffic volumes. The Dutch government also notes that Europe is not lagging behind other regions in terms of investment, despite differences across member states.[14]

However, the main debate is not about estimating how much network operators need to invest. It is about whether the market works well enough to provide adequate incentive for network operators to invest whatever amount is necessary to maximise benefits to society.

- On the one hand, network operators point to their declining returns to suggest that they lack incentives to adequately invest. Their revenues have been flat, despite the increase in data volumes and associated costs. In turn, that reduces their return. HSBC estimates that average ROIC (return on invested capital) for the major listed European telecommunication operators fell from around 8% in 2012 to around 5% in 2020 and that many operators now have returns below their cost of capital.[15] And the cost of capital has now increased with rising interest rates and increased stock market volatility.[16]

- On the other hand, declining returns do not necessarily imply that investment is under-rewarded or inadequate. Content providers argue that providing network infrastructure remains a highly profitable business, with increasing dividend pay-outs at a multiple of the average of European listed companies.[17] This view has been espoused by BEREC in their preliminary assessment of the issue, and by the Dutch government in the response to the EC consultation. BEREC notes that “the attractiveness of access network investment is reflected in the annually increasing capital investors’ investments in fibre access networks” and returns are relatively high given the level of risk that operators face.[18]

If there is underinvestment, what is the market failure?

To the extent that there is underinvestment, the second key question is what the reason for it is.

Ultimately, investment is not about “fairness”, it is about efficiency. If markets work well, one can expect network operators to respond with adequate investments to the increasing demands on network infrastructure, even if the cost of meeting that demand is large. If it is true that network operators underinvest, then there must be the market failure that explains that underinvestment.

Investments generate positive externalities

The market failure that network operators identify is that their investments generate positive externalities.

The European Telecommunications Network Operators Association (“ETNO”) explains that while their investments benefit other parties – particularly large content providers – network operators are not rewarded for providing those benefits; this is because content providers do not contribute to investment in infrastructure.[19] A commissioner at the US FCC recently noted in this vein that “the telecom revenues have been declining. At the same time, these large technology companies benefit greatly from these high-speed networks”.[20]

However, these externalities alone are not enough to explain underinvestment. Content providers, [21] BEREC [22] and the Dutch government [23] point out that network operators charge consumers directly for the data their infrastructure provides. If those consumers demand more data and network operators must invest to provide that service, then they should be able to invest adequately to the extent that consumers are willing to pay for the incremental benefit that additional investment offers. Consequently, content providers have argued that the Fair Share Proposal risks allowing network operators to charge two sets of ”customers” for the same services: once for the consumption of services that require data, and once for the provision of services that requires data.[24]

Essentially, the issue that the EC will have to unpick is how the price and consumption of internet access and content interact. Internet access and content are complements, as the price of one affects the demand for the other. In principle, if investment in infrastructure increases consumer demand for the services that rely on that network, then network operators should be able to recover those costs from their own customers. After all, anyone who values watching YouTube, Netflix, or any other data-dependent service (that currently exists, or will emerge in the future), also values access to the internet and pays for it (whether by money or by attention sold to advertisers). In practice, those interactions can be complicated. Network operators, for instance, argue that fierce competition across and within networks, as well as an increasingly common “flat” internet access fee that is not conditioned to network usage, prevent them from charging customers for their usage of the network and ultimately from capturing a fair share of the benefits their investment would create.

The EC will also have to consider that content providers’ investment in content and services drives traffic on the network, increases demand for internet access and indirectly benefits network operators. This means that any underinvestment assessment would have to account for the complex interdependence of network operators and content providers and the various externalities which emerge from it.

Potential externalities cannot be internalized through bilateral contracting

Even if the EC determines that network operators’ investments do generate spill-overs that their consumers do not adequately reward, there is an additional market failure that supporters of the Fair Share Proposal would have to demonstrate. General underinvestment would be likely to harm content providers that would otherwise enjoy those spill-overs. The problem with a positive externality is not that content providers benefit for free. It is that they benefit less than they would if they could incentivise the efficient level of investment. Absent an additional market failure, they should willingly agree to directly incentivise any additional investment that would benefit them. If they don’t, that may be telling.

Unsurprisingly, the reasons why network operators and content providers do not negotiate payments to bring forth investment is contested. Four potential barriers should reward scrutiny.

No problem to fix

The first reason is obvious and follows from the disagreement above: content providers argue that there is no underinvestment that they, or anyone else, need to finance.

Free-riding

The second potential reason is free-riding: if an individual content provider pays to improve the network and reduce congestion, then it benefits not only itself, but also its rivals who may not have contributed. In that case, the best strategy may be to let others pay for network improvements – whether by paying network operators, or by directly investing in undersea cables and Content Delivery Networks (hereafter “CDNs”) as some content providers have done – without contributing oneself. But if all providers follow that strategy, too few will invest adequately leading to higher network congestion. While investment has limited congestion to date, it is uncertain whether investment will remain sufficient in the face of ongoing growth in data demand.

Asymmetric information

The third potential reason is asymmetric information on the investment gap and its impact. It is unsurprising that each side of any bilateral negotiation – the telecommunications network operators on the one hand and content providers on the other – would have profoundly different views on the nature and extent of the issues. In particular, to reach an agreement, a content provider would need to trust a network operator’s assessment of the investment gap. But it lacks the information to verify that estimate and trust it. Similarly, a network operator would need to trust a content provider’s assessment of the spill-over effect (the impact that additional investment has on its profits). But it too lacks the information to verify that estimate and trust it. In that case, we would expect negotiations to break down, even between parties that would willingly agree to some payment if they could trust each other. Whether this is an important barrier is unclear.

Imbalanced bargaining power

The final potential barrier is imbalanced bargaining power between network operators and content providers. Network operators have little independent leverage to encourage content providers to negotiate. They are prevented by law from discriminating between types of content providers for commercial reasons (such as denying or degrading services to some providers’ services). Even if they could do so, the reaction from consumers would likely be strong – if an operator denied its customers access to YouTube or Netflix, it is more likely that its customers would switch internet providers than consume other different content. However, the doubt here is whether leverage matters by itself. The chief concern about underinvestment is that it harms all parties: content providers, network operators, and consumers. It is in all their interests to fill any shortfall.

BEREC appears to take this perspective. In its preliminary assessment, BEREC suggests that telecommunication operators and content providers are interdependent: the demand for internet content promotes uptake of internet access (and shifts demand to access products with faster speeds), which in turn enables greater demand for more data-intensive content. Interdependence, compared to one of imbalanced bargaining power, should facilitate an arrangement in theory. However, this leaves open whether such an arrangement would deliver the optimal level of investment and a charging structure that promotes efficient usage.

What are the options?

To the extent that there is a market failure, the third key question is how to remedy it.

Network operators have called for rules that oblige (large) content providers – or other digital players generating large amounts of traffic – to contribute a “fair share” to network costs.[27]

If that contribution is considered necessary, there are two practical challenges to address:

- how to establish the amount that content providers should pay (if at all); and

- how to verify that network operators fill the investment gap.

There are various options to address these two challenges.

How to establish the amount that content providers should pay (if any)

Broadly, there are three mechanisms to determine the efficient contribution to network costs:

- bilateral negotiation;

- bilateral negotiation backed by mandatory arbitration; and

- regulation.

There is also the option to do nothing, if there is no problem to fix – or if none of the above mechanisms is effective.

Bilateral negotiation

The simplest solution is to compel network operators and content providers to negotiate an adequate payment between themselves. The barriers to this approach are the three set out above: free-riding; asymmetric information; and imbalanced bargaining power. While they may not be a problem in practice (i.e., there may be no problem to fix, as the content providers argue), if operators underinvest, then at least one of these barriers must be a problem.

Compelling network operators and content providers to negotiate may mitigate their impact to an extent. For instance, no rival provider could dodge contributions entirely and each party in a negotiation will have to provide some information to explain its position. But the core issues would remain. Rivals might negotiate lower contributions and have incentive to do so. Negotiating parties have reason to embellish their own position and distrust their counterparty. Lacking competitive tension, we should expect that the outcome of negotiations in that context would reflect the parties’ relative bargaining power rather than the economic reality of any shortfall in investment and the scale of its spill-over.

In addition, that compulsory negotiation might shift imbalanced bargaining power rather than neutralise it. Both the CCIA and BEREC are concerned that mandating content providers to contribute to network costs could enable operators to “exploit the termination monopoly” (i.e., their control on final delivery of traffic to a consumer), potentially harming the development of the internet ecosystem and its services – for example, based on a loss of connection quality to a content provider in case of disputes.[28]

Bilateral negotiation, backed by mandatory arbitration

This second option seeks to mitigate the barriers to simple negotiation. It has been implemented in Australia and France to address a similar issue with externalities and underinvestment: the imbalance in bargaining power between news organisations and digital platforms.[29]

As above, each side must negotiate an agreement. However, should they fail to agree, the matter goes to an arbitrator who decides the outcome. In Australia, this takes the form of final offer arbitration, where each side must submit a final offer that arbitrators choose between. That deters parties from arguing extreme positions because the arbitrator would then be more likely to adopt the other party’s offer as more reasonable.

The rationale for compulsory arbitration is that it provides security to address the concerns above. Imbalanced bargaining power is mitigated, as the weaker party (whichever side that is) can request an independent judgment. Independent adjudication also limits rivals’ ability to free ride. Asymmetric information is less damaging to trust, as parties negotiate in the shadow of an independent assessment with powers to compel each side to provide information.

Regulation

A completely independent approach is regulation. A regulator could determine the payments that content providers should pay to network operators to contribute to the recovery of network investment. It would set the criteria to identify who should pay, and it would calculate their contributions based on the network investments and the benefits arising to network operators, content providers and consumers.

Practically, this approach is challenging to the extent that neither side of the debate might be satisfied with it. Regulators do not have perfect information. Gathering the vast amounts of information necessary to estimate efficient contributions would have high costs and administrative burdens. Furthermore, regulation may be too rigid in a context of fast-moving technological change and evolving user behaviour and may deter parties from reaching more efficient arrangements via negotiation.

Do nothing

Obviously, nothing should be done if there is no problem to fix. This view is reflected in BEREC’s preliminary assessment and CCIA’s position paper on the issue. It cannot be excluded that (in principle at least) doing nothing is the least bad option even if there is underinvestment. If the scale of the problem is less than any error that the mechanisms above introduce, then living with some underinvestment may be preferable to creating new problems.

How to ensure that operators fill the investment gap

The rationale for a change in charging regime is to promote investment. As such, even if payments are required, authorities will want to ensure that they actually generate higher investment. Below are some policy options, potentially with varying degrees of success.

- Bilateral negotiation. Simple negotiation may fail on this front. If the charging structure does not impact network operators’ investment incentives, then it will not solve the underinvestment problem. Seeking to achieve additional investment through contracts or other legal arrangements may instead raise difficult practical questions such as what investment the operator would have made anyway and how to deal with situations where market circumstances require changes in the amount and timing of investments.

- Access to a centralized fund administered by the regulator. Another option is regulation. A regulator could control operators’ access to a centralised fund of payments, conditional on verified and additional investment. Although the challenges and administrative burden of regulation are narrower for this option than they are for a regulator that also estimates the payments required, some challenges are likely to remain. In particular, it may be difficult for the regulator to identify and verify additional investments, that would not have occurred absent payments from content providers.

Conclusion

Technological developments, such as Artificial Intelligence (“AI”), the Internet of Things (“IoT”), the Metaverse, and innovations across a range of industries (autonomous vehicles and the greater use of robotics in manufacturing, for example) have the potential to revolutionize our lives. But they depend on adequate investment in the infrastructure that will enable them.

In that context, it is important that the “Fair Share” debate, and the factual questions around it, are resolved in a way that promotes efficient investment. It is not only about whether network operators and content providers should split the costs. It is also about whether the current market works or not. Either it encourages network operators to invest where those investments are socially beneficial, or it doesn’t. Ensuring that it works is in everyone’s interests: network operators, content providers (the ones we have, and the ones that could emerge in future), and consumers.

Read all articles from this edition of the Analysis

View the PDF version of this article

[1] Guillaume Duquesne is a Senior Vice President at Compass Lexecon. Cecilia Nardini is a Vice President at Compass Lexecon. Gabriele Corbetta is an Economist at Compass Lexecon. The views expressed in this article are the views of the authors only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients. Other Compass Lexecon economists have previously or are currently advising interested parties including network operators, content providers, and regulators on this issue. However, this article is independent of that advice, and not funded by any client. The authors advise and have advised both telecommunication companies and content providers on other matters, but they are not advising any companies on this particular matter, and have not previously done so.

[2] EC (2023), Consultation on “The future of the electronic communications sector and its infrastructure”, accessed May 2023.

[3] EC (2023), Survey from the exploratory consultation on “The future of the electronic communications sector and its infrastructure”, p. 39.

[4] Bertuzzi, L. (2023), “US telecom regulator throws his weight behind EU senders-pay initiative”, Euractiv, 23 May.

[5] Sandvine (2023), “2023 Global Internet Phenomena Report”, pp. 9 and 20.

[6] UK Parliament (2022), “Research Briefing: The impact of remote and hybrid working on workers and organisations”.

[7] Sandvine (2023), “2023 Global Internet Phenomena Report”, p. 14.

[8] Sandvine (2023), “2023 Global Internet Phenomena Report”, pp. 10-15.

[9] EC, “Support for Broadband rollout”, accessed May 2023.

[10] Ofcom (2022), “Ofcom’s future approach to mobile markets and spectrum”, p.14.

[11] ETNO (2023), “State of Digital Communications 2023”, p. 5.

[12] GSMA (2020), “Realising 5G’s full potential: Setting policies for success”, p. 3.

[13] Frontier Economics (2021), “Shaping Policies to Support Investment in Very High-Capacity Networks”, p. 13.

[14] BEREC (2022), “BEREC preliminary assessment of the underlying assumptions of payments from large CAPs to ISPs”, pp. 7-10. Dutch government (2023), position paper accompanying the consultation response “The future of the electronic communications sector and its infrastructure”, p. 4.

[15] HSBC (2021), “European Telecoms: Call to return (on capital)”, pp. 2, 7, 10.

[16] Mankins, M. (2023), “Capital Is Expensive Again. Now What?”, Harvard Business Review, 30 March.

[17] CCIA (2023), “Position Paper on Network Fees”, p. 4.

[18] BEREC (2022), “BEREC preliminary assessment of the underlying assumptions of payments from large CAPs to ISPs”, p. 13. Dutch government (2023), position paper accompanying the consultation response “The future of the electronic communications sector and its infrastructure”, p. 4. BEREC references a paper for the EC which focuses on investment in fibre and was completed before the sharp increase in interest rates last year.

[19] ETNO (2021), Joint CEO statement: “Europe needs to translate its digital ambitions into concrete actions”, accessed May 2023.

[20] Bertuzzi, L. (2023) “US telecom regulator throws his weight behind EU senders-pay initiative”, Euractiv, 23 May.

[21] See, for example, a quote from Christian Borggreen, head of CCIA Europe: Pollet, M. (2023), “Big Telco vs. Big Tech: The battle over ‘fair share,’ explained”, Politico, 20 February.

[22] BEREC (2022), “BEREC preliminary assessment of the underlying assumptions of payments from large CAPs to ISPs”, p. 14.

[23] Dutch government (2023), position paper accompanying the consultation response “The future of the electronic communications sector and its infrastructure”, p. 8.

[24] See, for example, Netflix (2021), “A cooperative approach to content delivery”, p. 7.

[25] CDNs are networks of servers which are geographically closers to users than the server hosting a website. CDN servers store or cache web content and make it available to users with improved speed and quality of delivery. See IBM, “What is a content delivery network (CDN)?”, accessed May 2023.

[26] BEREC (2022), “BEREC preliminary assessment of the underlying assumptions of payments from large CAPs to ISPs”, pp. 10-11.

[27] ETNO (2021), Joint CEO statement: “Europe needs to translate its digital ambitions into concrete actions”, accessed May 2023. See also Axon Partners Group (2022), report for ETNO: “Europe’s internet ecosystem: socio-economic benefits of a fairer balance between tech giants and telecom operators”.

[28] BEREC (2022), “BEREC preliminary assessment of the underlying assumptions of payments from large CAPs to ISPs”, p. 4. See also CCIA (2023), “Position Paper on Network Fees”, p. 3; and Netflix (2021), “A cooperative approach to content delivery”, p. 31.

[29] Saheli, R. C. (2021), “Australia passes new media law that will require Google, Facebook to pay for news”, CNBC, 24 February. See also Browne, R. (2021), “Google agrees to pay French publishers for news”, CNBC, 21 January.

Related insights

-

The Analysis • 13 Jun 2023

Use of runner-up evidence in merger assessments

-

The Analysis • 13 Jun 2023

The special merger regime for energy networks: lessons from the water sector

{kind=link}