Competitive Effects of Price Parity Agreements

Share

Competition authorities have been hostile towards price parity agreements. However, not all agreements are alike. Wholesale price parity agreements, like those observed in the airline ticket industry, can intensify competition, not fetter it—to the benefit of consumers. Salvatore Piccolo and Kadambari Prasad set out the different types of parity agreement and explain the factors that determine their impact on consumers.

View the PDF version of this article.

The views expressed in this article are the views of the authors only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

Platforms acting as intermediaries between buyers and sellers affect how competitive many industries are. They can help buyers find offers they would not otherwise see or would incur higher costs to discover. They can intensify competition among sellers by making their range of offers transparent. This is the bright side of platform intermediation. However, in some circumstances, platforms can also use their position to extract supra-competitive fees, thereby inflating the prices consumers pay. This is the dark side of intermediation.

Assessing how these platforms affect competition in any given industry is not easy. Their ability to manacle competitive forces will depend on various factors. Competition authorities, regulators, and courts on both sides of the Atlantic have turned their attention to one of those potential factors: price parity agreements – also known as ‘most favored nation clauses’ (MFNs).[2] These restrictive contracts reference rivals,[3] and prevent price competition with them. For example, if a hotel offers a price on one booking platform, a retail price parity agreement could prohibit the hotel from offering a lower price to consumers using other distribution channels, for example on a rival booking platform or the hotel’s own website.

Antitrust and competition authorities have been typically hostile towards price parity agreements and – in the case of “wide” retail price agreements, where the same retail price must be offered on all distribution channels – such hostility is well-grounded. In the absence of off-setting efficiencies, many scholars of economics have set out the detrimental impact that such contractual agreements can have on firms’ profits and consumers’ welfare. However, not all parity agreements are alike and their impact on consumers varies.[4]

In some circumstances, some types of parity agreements can be pro-competitive, benefiting consumers. In particular, wholesale price parity agreements – where a platform that connects wholesalers with specialist retailers prohibits the wholesaler from offering lower prices on rival platforms – can reduce retail prices, rather than increase them. For instance, the airline ticket distribution industry – which has recently attracted significant policy and regulatory scrutiny – is a clear example where these provisions are implemented and have enhanced competition, not hindered it.[5]

The distinctions between different kinds of parity agreements – and clarity on the circumstances in which each one is either beneficial or harmful – will be increasingly relevant as platforms of different shapes and structures emerge in various industries. Already, many industries feature business-to-business (B2B) platforms in a multi-layered structure. Similarly to wholesale platforms for plane tickets, that connect airlines and travel agents, wholesale platforms have emerged for agricultural and pharmaceutical products and in e-commerce (e.g., Amazon, Alibaba, TradeWheel, DHGate, and ECVV). Many of these platforms could attract attention from regulators and competition authorities in the future.

That attention should not presume that parity clauses are harmful per se. Nor that consumers’ interests are necessarily aligned with those of the sellers or necessarily in conflict with those of distribution platforms. Such approaches would be bound to produce too many errors, resulting in over-enforcement and harm to consumers’ interests.

Below, we outline different kinds of parity agreements and explain why their impact on consumers’ interests can vary depending on the circumstances in which they are applied.

The (often) negative competitive effects of retail-price parity agreements

We first review the dynamics that shape the competitive effects of the simplest restrictions: retail price agreements. We illustrate this with reference to the hotel booking industry assuming away off-setting efficiencies.

Pricing dynamics in the hotel booking industry

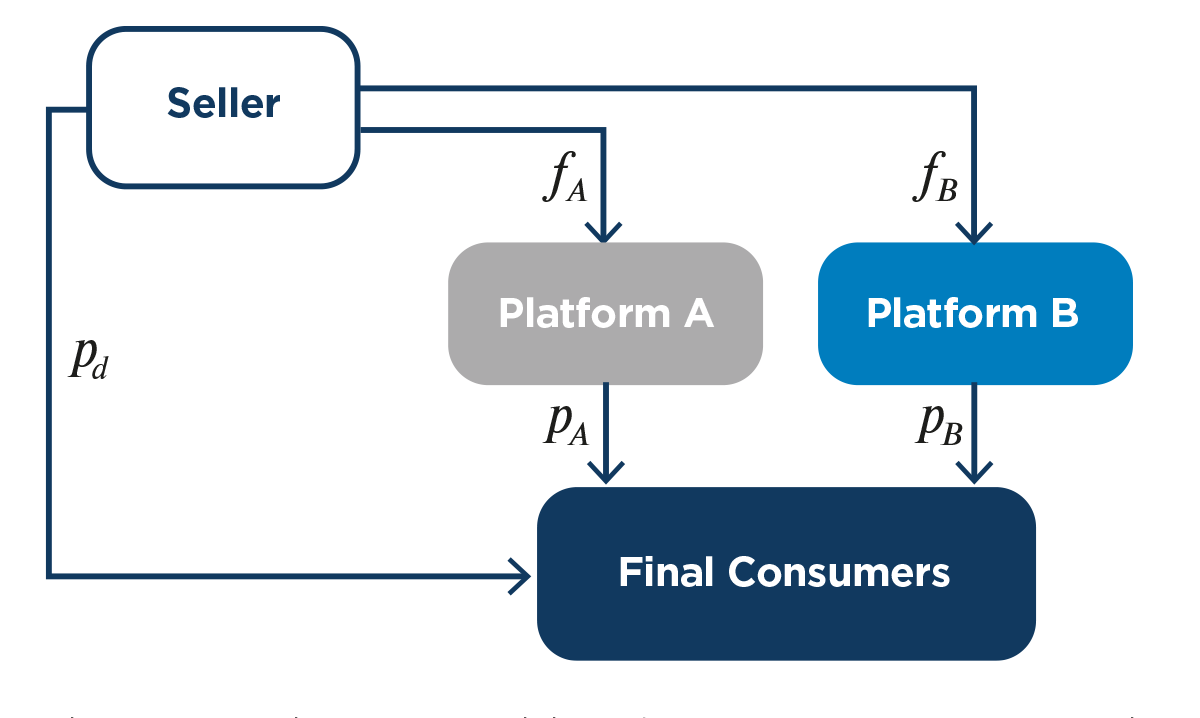

Consider intermediary platforms in the hotel booking industry – illustrated in simplified form in Figure 1 below. Consumers can purchase the same hotel room (a) directly, from a hotel through its website at price pd, or (b) indirectly, through a hotel comparison platform at price pA or pB respectively. Hotels pay a commission to booking platforms (fA and fB), in order to reach potential customers they might not otherwise reach.

Figure 1: The hotel booking industry

What must hotels and booking platforms consider when setting their commissions and retail prices? Each party, as in most industries, faces a trade-off between (a) the margin it can earn on each sale, and (b) the number of sales it can expect to make. In this context, that trade-off has two important elements.

First, higher margins can redirect customers to rivals. Each platform will consider how its commission may be passed through, in part, to retail prices downstream and the risk that high commissions will redirect its users to rival platforms or a rival distribution channel (i.e., hotels’ direct channel).

Second, higher margins can price out consumers, in that some customers will choose not to book hotel rooms at all. In any industry, a company seeks the optimum balance between margins and sales. However, companies in a multi-layered supply chain will struggle to find that balance. They can be encumbered with a “multiple-marginalization” problem – where the margins charged by the individual layers accumulate so that the aggregate margin generates lower aggregate profits than it would have done had the companies set lower margins and so attracted more customers.

How these two factors interact to determine a party’s pricing strategy will depend on circumstances. In particular, it matters (a) what the terms of the parity agreement are, and (b) whether consumers switch between platforms and distribution channels. For example, if customers are very loyal to a particular comparison site, that platform will be less worried about price competition than it would be if consumers used multiple platforms and freely switched between platforms and hotel’s direct channels depending on price.

Why “wide” retail price agreements are always bad

A “wide” retail price-parity agreement requires that sellers charge the same retail price on all distribution channels and platforms. That is, a platform only grants a hotel access to its users on the condition that the seller cannot undercut it on rival platforms (such that pA = pB = p)[6], nor when it sells directly to consumers through its own site (such that pd ≥ p).

Absent off-setting efficiencies, this kind of agreement will dampen price competition. It allows a platform to set higher commissions without losing its users to rival platforms or direct distribution channels. Even if rivals charge lower commissions (or have lower costs on their direct sales), they must offer the same price in each case. With such an agreement in place, a platform won’t fear price competition. It knows consumers will not be able to find lower-priced alternatives elsewhere; all channels offer the same good at the same price. In addition, new platforms will struggle to enter the market, as they will be unable to charge lower prices to entice consumers.

Platforms’ commissions are not entirely unconstrained. They still need to consider multiple marginalization (i.e., whether lower margins would increase aggregate profits by attracting more sales). However, by using a retail price parity agreement to increase its commissions, the platforms can shift the brunt of that problem onto the hotels.

Without a wide parity agreement, a hotel has a freer hand to set lower retail prices for sales in the indirect distribution channel, as price competition between platforms keeps their commissions low. If consumers freely switch between the two distribution channels, it might set a high retail price on the platform: redirecting many users to its more profitable direct channel and earning a decent margin on any users that remain on the platform. If consumers are loyal to platforms, it could set a moderate retail price without being strongly affected by the multiple marginalization problem (as the platforms’ share of aggregate profits is low).

Under the wide parity agreement, the seller has less room to maneuver. A high retail price on the indirect channel will not direct customers to its direct channel, as the agreement requires it to offer the same price on each distribution channel. In addition, its available margin on the indirect channel is much more squeezed than it was without the agreement. Higher platform commissions mean that it bears the brunt of multiple marginalization even if it sets only a moderate price – because its available share of the optimum aggregate margin is reduced. The net effect is that prices are higher, volumes are lower, and consumers are worse off.

Why “narrow” retail price parity agreements are (often) bad

A “narrow” retail price-parity agreement prohibits a seller from setting a cheaper price when selling its product directly, but – unlike wide agreements – they are free to charge i.e., lower prices on rival platforms.

This kind of agreement is likely anti-competitive (absent off-setting efficiencies) when (a) a seller must have access to a particular platform to reach its users (i.e., it is a ‘must-have’ platform) and (b) many consumers freely switch between direct and indirect channels depending on the prices they offer.

The reason is that a platform can set a high commission knowing that the ‘narrow’ parity agreement prevents the seller from using direct sales to undercut it. Although a seller could set a lower price on rival platforms (that charge lower commissions), it would be unwise to do so. That lower price would undercut both the high-commission platform and its own (more profitable) direct sales, which are tied to the price of the high-commission platform. As such, the narrow parity agreement, under these two conditions, will insulate a platform from competition and keep retail prices high. As before, the seller bears the brunt of double marginalization.

Narrow price-parity agreements will not be anti-competitive when sellers can “delist” themselves from a high-commission platform without incurring much cost. For example, if most of the consumers on a high commission platform also use rival platforms (referred to as “multi-homing”), then the former is not a ‘must-have’ platform. The seller can abandon it without losing access to many customers because it can reach them through cheaper rival platforms.

The (often) positive competitive effects of wholesale price parity agreements

Platforms can also intermediate between buyers and sellers in the wholesale layer of a supply chain. The airline ticket industry is a clear example and, as discussed, other B2B platforms are emerging.

Parity agreements in the airline ticket industry

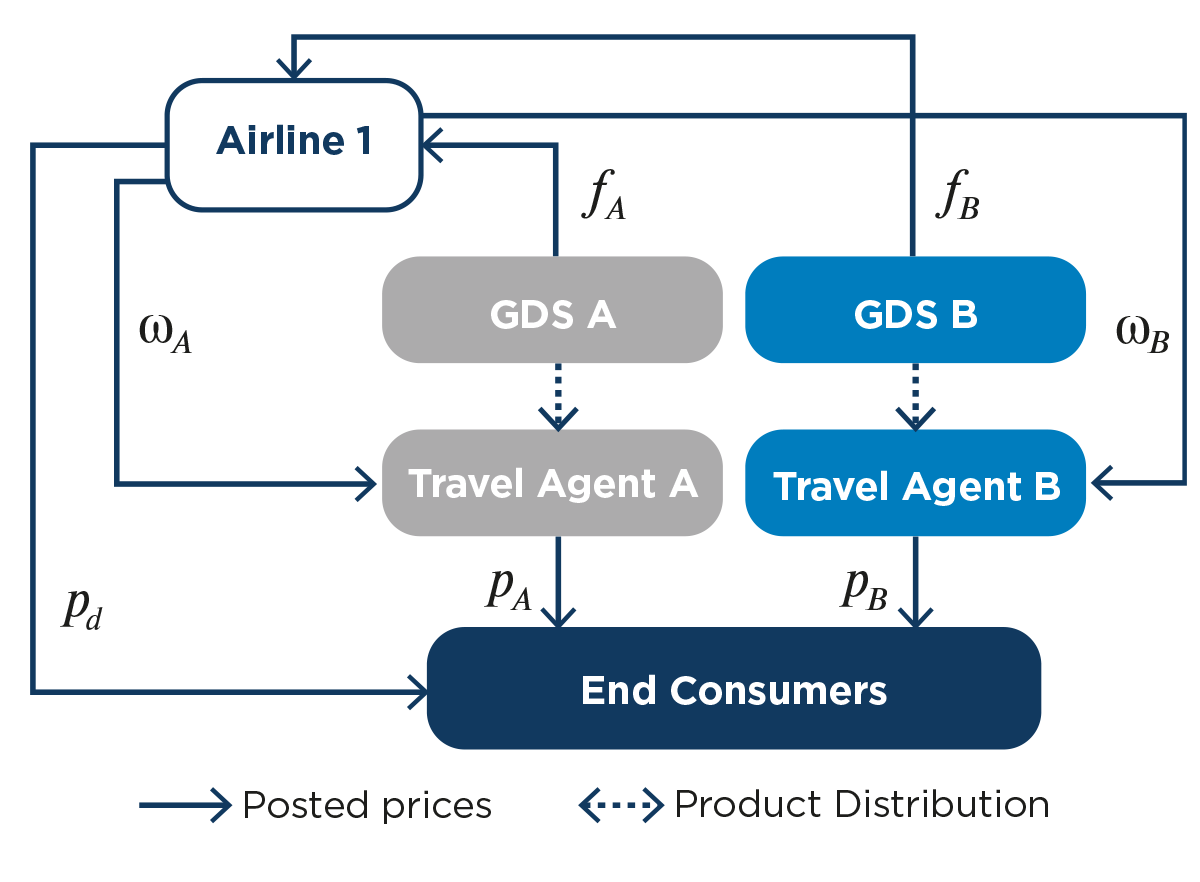

In the agency-based multi-layered industry – shown in simplified form in Figure 2 below – an airline can sell tickets to travel agents, via Global Distribution System (GDS) platforms, at wholesale prices wA and wB. In turn, travel agents sell those tickets to consumers at retail prices, pA and pB. The airline pays commission (intermediation fees, fA and fB) to the platforms, to access travel agents on the respective platforms GDS A and GDS B. They negotiate those commissions bilaterally and pass them on to travel agents via wholesale prices. In addition, the airline can also sell tickets directly to consumers, for example, through its website (at pd).

Figure 2: The agency model in the Airline Ticket Distribution Industry

The GDS platforms impose a different kind of parity agreement, relating to wholesale prices rather than retail prices. These restrictive clauses prohibit airlines from charging lower wholesale (or ‘input’) prices on rival platforms (i.e., they mandate wA = wB), but leave retail prices unfettered – either through an airline’s direct channel, or travel agents (pd, pA, or pB).

Why wholesale parity agreements can be procompetitive

How does a wholesale parity agreement change pricing dynamics? Sellers and platforms still consider their trade-off between margins on each sale and the volume of sales. However, there is an important difference: the parity agreement only constrains price competition between wholesale platforms and not between distribution channels. If a sufficient proportion of consumers switch between indirect and direct distribution channels, then the seller’s direct sales will impose a competitive constraint on the margins and prices that platforms and travel agents can profitably pursue in the indirect distribution channel.

To appreciate why, consider how that difference alters platforms’ and sellers’ incentives when setting commissions and prices.

First, consider a platform’s incentives when setting its commissions. As before, without a parity agreement, it anticipates the airline will pass on whatever commission it charges. If the platform sets a higher commission than its rival platform, (such that fA > fB), the airline will reflect that incremental cost in the wholesale price it charges to travel agents using that platform (such that wA > wB). Only the platform is disadvantaged by the high wholesale price, not the airline since both anticipate that travel agents will divert their trade to a cheaper platform and the airline will maintain its indirect sales through that rival. Fearing price competition, platforms will set relatively more competitive commissions without a parity agreement.

With a parity agreement, price competition between platforms reduces, and so platform commissions will likely be higher than without an agreement. That is because neither platform will fear losing its customers to a rival, as by contractual agreement, no other platform can be offered lower wholesale prices.

However – unlike the hotel booking platforms that imposed retail price agreements – the wholesale platforms are exposed to the impact of retail price competition between travel agents and the airline’s direct sales channel. That changes their calculus when setting commissions. If they set high commissions and those commissions increase the retail prices that travel agents charge downstream, then they risk losing profits. Price-sensitive customers might switch to the airline’s cheaper direct distribution channel. Therefore, to the extent that sales downstream from wholesale platforms are exposed to competition from direct sales, platforms will have to be more cautious about imposing high commissions on sellers than they would be if retail prices were constrained.

Second, now consider how the wholesale price parity agreement changes the seller’s incentives when it sets a wholesale price in the indirect distribution channel and sets retail prices in its direct channel.

As before, under the parity agreement, the seller bears the brunt of double marginalization, this time exacerbated by a third layer (travel agents). All else being equal, the airline will be cautious about passing on commissions or applying its own high margin on indirect sales, as that would further reduce sales and profits through the indirect distribution channel.

However, unlike before, the seller is not beholden to the commissions that platforms set. It can retaliate by lowering retail prices in the direct sales channel to undercut retail prices in the indirect channel. A lower retail price benefits the airline in two ways: (a) it attracts customers to its relatively more profitable direct channel; and (b) the intensity of that competition will force wholesale platforms to reduce their commissions to remain competitive, and therefore reduce the negative impact that multiple marginalization has on the airline’s profits from indirect sales. This reduces retail prices in both channels, and therefore all consumers benefit.

Which circumstances determine whether an agreement is pro-competitive?

Whether or not the wholesale parity agreement is pro-competitive will depend on the seller’s incentive and ability to compete on retail prices.

The seller’s incentive to aggressively compete on retail prices is greater with a parity agreement in place than it is without one. Without a restrictive agreement, the airline would not need to drive down platforms’ commissions – as wholesale price competition between the platforms already keeps them low – and its own margins would be healthy across both channels. Under the parity agreement, it faces the brunt of multiple marginalization because its margin in the indirect distribution channel is squeezed to a greater extent.

The seller’s ability to use retail prices to defend its interests will depend on how freely consumers switch between distribution channels (i.e., on the extent to which they perceive the alternative distribution channels as substitutable).

If most consumers freely switch between the two channels, the airline will be in a stronger position. Indirect sales are contestable, so it has more potential to increase its direct sales. The wholesale platforms, in turn, face more intense pressure to reduce their commissions to protect their downstream sales. That gives the airline more freedom to choose between taking a bigger share of the profit on indirect sales and growing its sales in that channel with lower prices.

In contrast, if few consumers switch between the two channels, then the airline is in a weak position. Without competitive pressure from its direct channel, it has little ability to deter GDS platforms from setting higher commissions. In addition, passing on those commissions and adding its own high margins on wholesale prices would only exacerbate the multiple marginalization problem, increasingly pricing out potential customers and reducing sales and profits. This is closer to the situation that hotels found themselves in when booking platforms imposed retail price parity agreements.

So, what is the situation in the airline ticket industry? Like most industries, it has a mix of both forces. Some consumers prefer travel agents. Some prefer purchasing from airlines directly. Others switch between the two channels. Therefore, airlines have an incentive to pursue sales in both channels, and a range of sources demonstrate that competition between indirect and direct distribution channels is sufficient for them to pursue that strategy. For example:

- a recent International Air Transport Association (IATA) survey shows direct sales grew at the expense of indirect distribution channels between 2015 and 2019;[7]

- (before the pandemic) carriers expected to see around 45% of their reservations coming through their own online, direct channels by 2021, up from around 35% in 2016; and

- the Lufthansa Group recently stated that the percentage of bookings processed by its direct channels or through application programming interface-based connections hit 52 percent in 2019 up from 45% in 2018, and just 30% in 2015. In addition, Lufthansa expects further direct booking gains for its network airlines as it expands an initiative to push additional price points exclusively through direct channels.[8]

What does that mean for consumers? In these circumstances, wholesale price parity agreements will reduce retail prices and increase consumers’ welfare because a sufficient proportion of consumers switch between distribution channels. The wholesale parity agreement forces the airline to drive down prices in both distribution channels (a) to attract customers to its (relatively) more profitable direct sales channel and (b) to maximize its indirect sales, by driving down platforms’ commissions and limiting wholesale prices to mitigate the multiple marginalization problem and increase its volumes and profits. If an insufficient proportion of consumers were prepared to switch between the two channels, the parity agreement would likely harm their interests, keeping retail prices high.

Clearly, sellers won’t welcome wholesale parity agreements. Without these constraints, they would make greater profits, but consumers would be worse off. The only way to increase consumers’ welfare is to allocate more power to the wholesale platforms, to force the airlines to pursue a retail price war between distribution channels.

On that basis, we cannot prejudge what impact wholesale parity agreements will have in a given market. The facts and the dynamics of that market must be analyzed.

View the PDF version of this article.

[1] The views expressed in this article are the views of authors only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees, or its clients. Part of this article is based upon Michele Bisceglia, Jorge Padilla & Salvatore Piccolo, When Prohibiting Wholesale Price-Parity Agreements Harms Consumers, (2021), INTERNATIONAL J. of INDUSTRIAL ORGANIZATION, 2021. That study was commissioned by Amadeus.

[2] For example, in 2017, the European Commission and ten national competition authorities published a joint report on online travel agents and the price practices in the travel industry. The report's primary focus was the impact on prices and commission rates of the removal of parity or `most-favoured-nation' clauses in European countries.

[3] Scott Morton, F. (2012). Contracts that Reference Rivals. US Department of Justice, available at: www.justice.gov.

[4] Andre Boik & Kenneth S. Corts (2016) set out the anti-competitive effects of price parity clauses; as does Justin P. Johnson, The Agency Model and MFN Clauses, 84(3), THE REVIEW OF ECONOMIC STUDIES, 1151, 1185 (2017). The anti-competitive nature of price-parity provisions is challenged by Bjørn O. Johansen & Thibaud Vergé (2017), who find that consumers benefit from the introduction of a narrow or a wide price-parity clause provided that sellers can delist from platforms charging excessively high commissions. The regulatory aspects associated with retail price parity are explored in a recent paper by Renato Gomes & Andrea Mantovani, Regulating Platform Fees under Price Parity, mimeo, (2020).

[5] For example Michele Bisceglia, Jorge Padilla & Salvatore Piccolo, When Prohibiting Wholesale Price-Parity Agreements Harms Consumers, (2021), INTERNATIONAL J. of INDUSTRIAL ORGANIZATION, 2021, show that wholesale price parity unambiguously benefits consumers. See also Jeanine Miklos Thal and Greg Shaffer, Input Price Discrimination by Resale Market, RAND JOURNAL OF ECONOMICS, (2020).

[6] Note that pA = pB, rather than pA ≤ pB, rather than as both platforms insist on the agreement

[7] See Phocuswright, “Evolution of Air Distribution: New Distribution and Retailing Models (Part 3)”, (2019).

[8] See The Beat, “Lufthansa Group's Direct Booking Share Surpasses 50 Percent”, (2019).

Related insights

-

Article • 17 Aug 2021

Q&A: Competition and antitrust issues in digital markets

-

{kind=link}

{kind=link}