Have European authorities been stricter with tech mergers?

Share

In this article, Kirsten Edwards-Warren [1] analyses the difference between the CMA’s and EC’s decisions on tech mergers and their decisions on mergers in other sectors. She concludes that the challenge with tech mergers is not that their economic features necessarily increase risks to competition; the challenge is that those features make assessment of both the potential risks and the potential benefits more uncertain, and therefore, require detail and rigour in each case to ensure merger control serves consumers effectively.

The views expressed in this article are the views of the authors only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

Introduction

Both the EC and CMA have been explicit about prioritising digital markets, which are now clearly the focus of their regulatory activities and antitrust investigations – more than half of the EC’s open A102 investigations involve big tech companies. It is less clear whether they have taken a stricter approach to assessing and where necessary remedying mergers in tech markets.

In this article, we take a broader look at how the CMA and the EC have treated mergers and acquisitions in tech markets since the start of 2017. At Phase I, both authorities have approved tech mergers unconditionally roughly as often they have for mergers in other industries. However, we also find that most of the tech mergers that the CMA did not approve unconditionally at Phase I were subsequently cancelled or prohibited, and there were no tech mergers resulting in Phase I undertakings in lieu of reference (UILs): this was not the case for mergers in other industries. That tentative trend is much less pronounced in EC decisions.

How might these trends develop? We all recognise that the CMA, in particular, sees tech mergers as posing additional challenges, as set out in the 2019 report it commissioned on digital mergers.[2] But the challenge with tech mergers is not that their economic features necessarily increase risks to competition. The challenge is that those features may increase both the potential risks and the potential benefits, and the magnitude of each. That makes merger assessment more uncertain, and requires detail and rigour in each case to ensure merger control serves consumers effectively.

A comparison of merger outcomes in tech markets with other markets

How do the CMA’s decisions on tech mergers differ from those in other sectors?

Although it isn’t straightforward to analyse how the CMA treats those two groups of cases, we can use its industry classifications as a guide. The CMA classifies mergers that we conventionally refer to as tech mergers as occurring in the “electronics industry” (for example, Meta (formerly Facebook) / Giphy and Google / Looker Data Sciences), “communications” (such as Meta / Kustomer and Taboola / Outbrain), or “telecommunications”. For the analysis below, we identified all cases that were closed between January 2017 and June 2022 and were labelled in one of the three categories. To establish a group of tech cases in that period, we inspected each one and removed irrelevant cases – that predominantly related to communication infrastructure or media markets, such as Bauer Media group. We then reviewed the list of non-tech cases to identify any that would be better classified as tech cases. We identified six potential cases all classified as in the “distribution and service industry” category and chose to define one of them – Sabre / Farelogix – as a tech merger.[3]

We find that, at Phase I, the CMA does not appear to have been stricter with mergers in tech markets than it has been with those in other markets. Of the mergers that we classified as occurring in tech markets, the CMA cleared 67% of them unconditionally at Phase I (14 out 21). This is similar to the proportion that were approved unconditionally in cases in other industries (Figure 1).

In contrast, it is striking that no Phase I undertakings in lieu of reference (UILs) were accepted in tech cases; and that five of out of the seven tech cases that went to Phase II were cancelled or prohibited: Nvida / Arm, Taboola / Outbrain, and Thermo Fisher Scientific / Roper Technologies were cancelled; and Tobii AB / Smartbox Assistive Technology and Sabre/Farelogix were prohibited. Although we should be mindful not to over-interpret patterns in small sample sizes, we shall observe with interest how this potential trend develops.

Figure 1: CMA merger decisions between January 2017 and June 2022

Source: Compass Lexecon analysis based on data from CMA data on its decisions

How do the EC’s decisions compare?

The EC categorises its cases differently to the CMA, but we can apply a similar approach to compare its decisions for tech mergers with those in other industries. The EC uses the Statistical Classification of Economic Activities in the European Community (known as “NACE” codes), which is a much more granular taxonomy. At the highest level of aggregation, “information and communication” is the closest category to digital or tech industries. However, it is a varied group, including software publishing and information technology activities on the one hand, and book publishing and motion picture and sound recording activities on the other. To aid comparison with the CMA analysis, we took a narrower group of subcategories, comprising software publishing (division J.58.2); computer programming, consultancy and related activities (division J.62.0); data processing, and hosting and related activities; and web portals (division J.63.1). We also included manufacturing codes related to electronics (divisions C.26.1 to C.26.4).

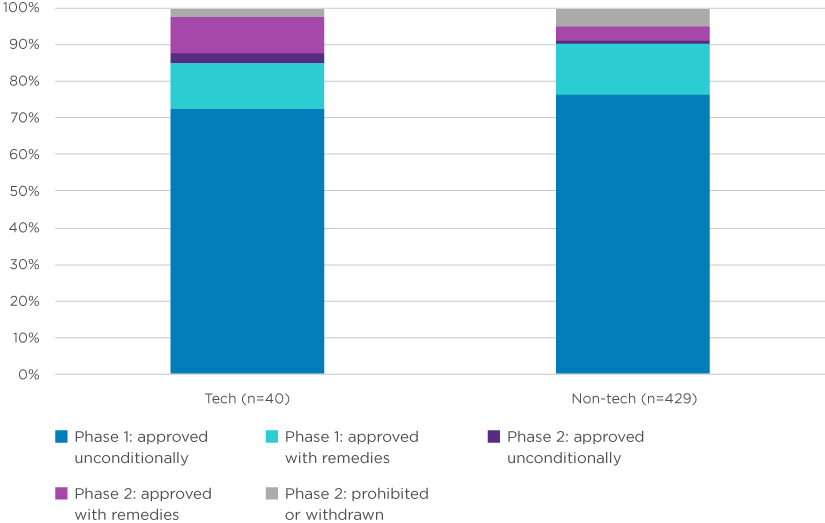

We find that the EC’s decisions on tech mergers are similar to its decisions in other sectors. Figure 2 shows that the EC cleared 73% of tech cases unconditionally at Phase I (29 out of 40) and 76% of non-tech cases at the same stage (not including Simplified Procedure). Furthermore, in contrast with the CMA’s decisions, there is no significant difference between the distribution of outcomes for mergers in tech industries and the distribution for mergers in all other industries: there were slightly more cases at Phase II, most of which are approved with remedies.

Figure 2: EC merger decisions, excluding Simplified Procedure, between January 2017 and June 2022 [4]

Source: Compass Lexecon analysis based on data from Compass Lexecon Decision Analysis Tool and the EC website

There are obvious limitations with attempts to define and monitor a tech sector. These markets are already very varied. Looking at the four mergers for which the EC required remedies after a Phase II investigation, their industries differ substantially. Qualcomm / NXP related to semiconductors; Thales / Gemalto to hardware security modules; Google / Fitbit to advertising, wearable devices, and health tracking apps; and Meta / Kustomer focussed on software for customer relationship management and messaging services. Little unites all four, and each has parallels closer to some non-tech mergers than they do to other tech mergers. And the number of markets we might categorise as a tech industry will only grow, as more economic activity becomes digital. Financial services increasingly provide digital services, as do transport and energy.

Even so, the similarity between decisions for tech mergers and decisions for mergers in other sectors is surprising. Not because we expect authorities to hold these mergers to a higher standard, but because they are more likely to have underlying economic features that are more challenging for authorities to assess.

The economics features that often make tech mergers challenging to assess

In the CMA’s 2019 assessment of its merger control decisions in digital markets, the CMA didn’t define digital markets. It specified economic features that those markets typically exhibit, and that can pose a threat to competition. In particular, the report sets out the challenges posed by network effects, multi-sidedness, big data and rapid innovation. We can add economies of scale and scope to that list.

Economies of scale and scope

Economies of scale occur when average costs fall as sales increase. This effect can be enormous in digital sectors, as the amount of money a firm spends on research and development and polishing its brand is considerable, but the incremental cost of selling an additional device or software programme is minimal – and potentially trivial.

Economies of scope occur when combining services reduces the average cost of providing them. For instance, where two products share research and development costs, it is cheaper for one company to provide both, than two companies to provide each of them separately. This is common in digital sectors, as once a company has already provided a set of services to its customers it can be cheaper to offer them additional services – compared with several companies building brands and services for each service separately.

These forces cause a dilemma for authorities assessing a potential merger. A single firm supplying the whole world would be the most efficient arrangement absent the negative effects of market power, but it increases the risk of market power emerging. Fragmenting the markets between rivals – or separating ecosystems into discrete products – would prevent concentration, but increases the costs that inevitably are passed on to consumers and reduces the return on investment.

Network effects and multi-sided markets

Network effects are the most significant feature identified by the CMA’s 2019 assessment. They occur when users of a product or service value its other users, not just the product or service itself. For instance, social media platforms are valuable when they have users you want to socialise with, not (just) because they provide a good method for communicating with them.

Multi-sided markets generate network effects between different users. For instance, app developers value an app store with many users, and those users value app stores with many developers. Online marketplaces are similar. Markets with many retailers attract potential customers, and sites with many customers attract retailers.

Multi-sidedness complicates merger assessment because the network effect needs to be taken into account in analysing market definition; pricing incentives and efficiencies - testing the ability of the standard analytical toolkit. There is not yet consensus among authorities on how multi-sided markets should be analysed, as evidenced by the opposing outcomes of the Sabre/Farelogix transaction which was approved by the DOJ on the basis that a one-sided firm cannot compete in a two-sided market, [5] but prohibited by the CMA on the basis that the firms were competitors in particular in respect of innovation.

Rapid innovation

Tech markets are often characterised by rapid innovation. This means that (a) market evolution is very difficult to predict, making it challenging to establish counterfactuals; and (b) there are huge potential synergies from acquisitions which authorities must be careful not to prevent. Acquisition can encourage innovators to join the race to invent the “Next Big Thing”. The reward of a buyout is an obvious incentive. Acquisition offers a clear route to market that circumvents the barriers that network effects can erect – as the entrant is brought into the ecosystem, rather than fighting to replace it.

However, that process can also deter competition to invent the next breakthrough. One concern is that an acquirer will “kill” the company it acquires to protect its extant profits. That phenomenon has been observed in the pharmaceutical industry, [6] and although it manifests differently in tech industries – where companies typically acquire start-ups in adjacent markets to expand their ecosystem, rather than horizontal competitors [7] – that acquisition can still help entrench an ecosystem against competition.

Another concern is that, even if buyout propels a race to be acquired, once a company wins that race the shadow of its acquisition might form a “kill zone”, deterring further investment. Third parties developing similar products may see little prospect of success competing against the acquired rival, and their own hopes for acquisition may be thwarted. In addition, the acquiring party may shut down its own research as it has paid to catch up – a phenomenon known as a “reverse killer acquisition”.

These economic features are reflected in recent decisions

There are signs these economic features have growing prominence in merger assessments, and the challenges they pose have featured in recent adverse decisions by the CMA and by the EC.[8]

For example, the CMA’s decision on Meta / Giphy is instructive (although it is not included in the data above, as CMA’s metadata still listed it as an open case at the time of analysis).[9] That the CMA investigated the acquisition at all is noteworthy. The parties didn’t notify the CMA, and neither the European nor American competition authorities investigated the purchase. Additionally, the CMA was motivated by both horizontal and vertical concerns about the impact on potential competition: that Giphy would have become a major competitor in display advertising (based on pre-merger trials that Meta terminated after the acquisition); and that Meta would completely or partially foreclose Giphy from competing social media platforms, diminishing competitors to Facebook.

The text of its final decision shows how those concerns are rooted in the underlying economic concepts set out in its 2019 report:

- a. It refers to network effects 48 times and multi-sided networks (two sided or otherwise) 17 times. And it refers to multi-homing 33 times, which can neuter the power of even large multi-sided markets.[10] For instance, noting that “multi-sided platforms such as Facebook are often characterised by network effects, in that the value of the product for users on one side of the platform depends on the number of users either on the same side of the platform, or on the other side.”

- b. It refers to the difficulties posed by non-monetary pricing 24 times. For instance, noting that “the nature of two-sided markets is such that a provider may offer its services below cost, or free of charge, to one side of the market while monetising the other side. This in itself is not informative of whether the provider has market power in one or both sides of the market.”

- c. It also refers to the impact that data has on competition between rival services 21 times. For instance, judging that “the desire to target specific audiences effectively means that the use of user data is key for display advertising, significantly more so than for search advertising. Consequently, access to granular user data is a key dimension of competition between display advertising suppliers.”

The EC is also adapting its approach to assessing mergers with the economic characteristics described above.

For example, it recently prohibited Illumina – a supplier for genetic and genomic sequencing – from acquiring Grail, a customer of Illumina that develops blood tests for the early detection of cancer.[11] The specifics of the Illumina/Grail transaction highlight two aspects of tech mergers that bear emphasis.

First, Illumina / Grail was the first case referred to the EC using the recent amendment of Article 22 of the EU Merger Regulations, which allows a wider range of mergers to be reviewed, even where they do not meet the thresholds for referral. The amendment intends to address concerns about potential “killer acquisitions” – loosely defined, so that it includes the acquisition of companies in adjacent markets, rather than ones that might have otherwise gone on to compete directly (i.e., horizontally).

Second, it is neither clear, nor revealing, whether this transaction is a tech merger or not. What matters is how the underlying economics made an assessment of their effect on competition challenging. The theory of harm that concerned the EC related to how the market for early cancer detection tests would develop. It concluded that “while there is still uncertainty about the exact results of this innovation race and the future shape of the market for early cancer detection tests, protecting the current innovation competition is crucial to ensure that early cancer detection tests with different features and price points will come to the market”. Analysing how competition will develop is inherently uncertain. In the U.S., the FTC’s objections to the acquisition were dismissed by the courts.[12]

The economic characteristics of tech mergers don’t necessarily increase competition risk; but they do increase uncertainty

What should we expect from merger assessments, particularly in those cases where the challenging economics of mergers in tech markets are most prominent?

Three lessons emerge:

- These challenges are common in tech markets but not unique to them. Network effects – and multi-sided markets – are challenging, but they are not new challenges. The fundamental mechanisms are well described by economists. The market for credit cards shows the complex and counterintuitive effects of two-sided markets and the lack of consistency across authorities’ decisions. The scale of those effects may be greater than before. But the tools and principles that helped competition authorities assess and understand those effects in the past, will help them again in the future.

- These challenges increase the cost of error, of both under-enforcement and over-enforcement. The CMA’s 2019 report notes that assessments will err. Incorrectly clearing mergers incurs costs. So does incorrectly intervening in them. The report notes that merger policy has, in its view, put too much weight on avoiding the incorrect interventions, and that the nature of competition in many digital markets may change the trade-off, particularly as network effects make incumbents harder to challenge. That is true. But it also increases the cost of incorrectly preventing beneficial network effects from emerging. The nature of network effects is that all users value them.

- These challenges increase the risk of error, in both directions. Assessing the impact that mergers with these characteristics have on competition is hard; even harder than normal, because of the speed at which markets evolve. Absent the merger, it is unlikely that the market will remain as it is. Authorities need to identify a plausible counterfactual to the merger, assessed over a reasonable time frame, to judge which scenario better protects competition and benefits consumers. That is hard. Business models can change or differ depending on whether or not the merger goes ahead. Predicting the dynamics of tech industries is particularly difficult, as network effects can tip a market rapidly. Without the benefit of hindsight, few would have predicted that Instagram would constitute a quarter of Facebook’s revenues by 2019. Even in retrospect, it’s hard to assess what would have happened absent that merger (Twitter was reportedly interested in acquiring Instagram, and we are watching how that business develops with interest).

These lessons matter. The interesting thing about tech mergers is not that they pose new challenges. It is that they increase the magnitude and impact of uncertainty.

One suggestion that has been floated to address this uncertainty is that we reverse the burden of proof – so that parties must prove that their merger will not harm competition, as opposed to the authorities proving that it will.[13] It is motivated by the view that merger control has been too lenient and that mergers bring little benefit. Essentially, this means arguing that incorrect clearances are prevalent and harmful, and that replacing those errors with incorrect prohibitions would be a relatively costless alternative.

However, when errors are likely and costly in both directions, we gain little from debating who ought to have the benefit of the doubt. We would be better served by focusing on how to reduce that doubt in the first place, and what to do when uncertainty remains. That will require rigorous assessment of both the underlying issues and the facts of the particular case.

Read all articles from this edition of the Analysis

[1] With thanks to the Compass Lexecon EMEA Research Team for analytic support. The views expressed in this article are the views of the author only and do not necessarily represent the views of Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

[2] The Competition and Markets Authority, Assessment of merger control decisions in digital markets, (3 June 2019). Available at: https://www.gov.uk/government/publications/assessment-of-merger-control-decisions-in-digital-markets.

[3] “Electronics” cases we classified as “tech”:

(1) Salesforce.com, Inc. / Tableau Software Inc merger inquiry; (2) Open International / Transactor Global Solutions merger inquiry; (3) Tobii AB / Smartbox Assistive Technology Limited and Sensory Software International Ltd merger inquiry; (4) Advanced Micro Devices, Inc / Xilinx, Inc merger inquiry; (5) NVIDIA / Arm merger inquiry; (6) Google LLC / Looker Data Sciences, Inc merger inquiry; (7) CGI Group / SCISYS Group merger inquiry; (8) SK hynix / Intel's NAND and SSD business merger inquiry; (9) Electro Rent Corporation / Test Equipment Asset Management and Microlease merger inquiry; and (10) Thermo Fisher Scientific / Roper Technologies merger inquiry.

“Communications” cases we classified as “tech”:

(11) ZPG / Websky merger inquiry; (12) Facebook, Inc./ Kustomer, Inc.; (13) Nielsen / Ebiquity merger inquiry; (14) Turnitin / Ouriginal merger inquiry; and (15) Taboola / Outbrain merger inquiry. (16) DMG Media Limited / JPIMedia Publications Limited merger inquiry; (17) Aragorn (KKR & Co Inc)/OverDrive Holdings Inc merger inquiry; (18) BT Group / IP Trade merger inquiry

“Telecoms” cases we classified as “tech”:

(19) Moneysupermarket.com Financial Group Limited / Decision Technologies Limited; (20) Sinch Holding AB / SAP Digital Interconnect Unit from SAP SE merger inquiry.

Non-tech cases reallocated to “tech”:

(21) Sabre / Farelogix merger inquiry.

[4] We have excluded Simplified Procedure cases for comparison with the CMA decision. There were 162 “tech” cases approved by the Simplified Procedure during the period, and 1423 other cases. “Tech” cases are all cases that the EC classifies using the NACE codes as: J58.2, Software publishing; J62.0, Computer programming, consultancy and related activities; and J63.1, Data processing, hosting and related activities; web portals; Manufacture of electronic components and boards (C.26.1); Manufacture of computers and peripheral equipment (C.26.2); Manufacture of communication equipment (C.26.3); and Manufacture of consumer electronics (C.26.4) (including subcodes within these categories). All cases are both notified and closed between 1 January 2017 and 30 June 2022.

[5] Following the Supreme Court of the United States, Ohio v American Express, 838 F. 3d 179, affirmed (June 2018). Available at https://www.supremecourt.gov/opinions/17pdf/16-1454_5h26.pdf.

[6] Colleen Cunningham, Florian Ederer, and Song Ma, “Killer Acquisitions” in Journal of Political Economy Vol. 129, No. 3 (March 2021). Available at: https://www.journals.uchicago.edu/toc/jpe/2021/129/3.

[7] Mats Holmström, Jorge Padilla, Robin Stitzing, and Pekka Sääskilahti, “Killer Acquisitions? The Debate on Merger Control for Digital Markets” (2018). 2018 Yearbook of the Finnish Competition Law Association. Available at SSRN: https://ssrn.com/abstract=3465... or http://dx.doi.org/10.2139/ssrn.3465454.

[8] The CMA’s decision on Meta/Giphy was subsequently appealed, and a revised final order is due in December. The EC’s decision on Illumina/Grail is subject to appeal.

[9] The Competition and Markets Authority, Facebook, Inc (now Meta Platforms, Inc) / Giphy, Inc merger inquiry. All documents available at: https://www.gov.uk/cma-cases/facebook-inc-giphy-inc-merger-inquiry#final-report-1.

[10] Survey Evidence on Multi-homing in Online Retail Businesses, John Davies, Sergey Khodjamirian, Felix Giallombardo and Pietro Aletti. Available at: https://www.compasslexecon.com...

[11] European Commission, “Mergers: Commission prohibits acquisition of GRAIL by Illumina”, 6 September 2022. Available at: https://ec.europa.eu/commission/presscorner/detail/en/ip_22_5364.

[12] The Federal Trade Commission, Illumina, Inc., and GRAIL, Inc., In the Matter of. All documents available at: https://www.ftc.gov/legal-library/browse/cases-proceedings/201-0144-illumina-inc-grail-inc-matter.

[13] Tommaso Valletti, “How to Tame the Tech Giants: Reverse the Burden of Proof in Merger Reviews” (June 2021). Available at: https://www.promarket.org/2021/06/28/tech-block-merger-review-enforcement-regulators/.

Related insights

-

The Analysis • 23 Nov 2022

Survey Evidence on Multi-homing in Online Retail Businesses

-

Article • 03 Oct 2022

A Missed Opportunity: The European Union's New Powers Over Digital Platforms

-

Article • 28 Jun 2021

The proposed DMA – Back to the “form-based” future?

{kind=link}

{kind=link}