Expert Q&A on Vertical Merger Enforcement

Share

Expert Economist Andy Parkinson participated in a Q&A with Financier Worldwide, joining lawyers from Baker Botts, Hogan Lovells, and Latham & Watkins LLP, providing a UK and EU perspective on recent developments in vertical merger enforcement.

Could you provide an overview of how vertical mergers are generally treated for antitrust enforcement purposes?

Parkinson: Most vertical mergers do not raise competition concerns and can instead result in efficiencies. If a downstream company purchases its upstream supplier, instead of paying a wholesale price for the inputs, it can instead access those inputs at cost, which would enable it to offer lower prices to its own customers. In addition, vertical integration can align incentives within the merged firm to invest in new products. However, the upstream supplier will often also sell to competitors of the downstream company. Enforcement agencies may be concerned that post-merger, the merged entity might use its control of an important input to harm its downstream competitors, by charging higher prices to those competitors or by stopping supplying them altogether, and this could reduce competition in the downstream market. This is called input foreclosure. Less commonly, customer foreclosure might be a concern: post-merger, the downstream company might switch its purchases away from other suppliers to its own upstream division. If the downstream company is an important customer for other suppliers, the loss of sales suffered by other upstream suppliers might mean they become less effective competitors.

Drilling down, could you outline the principal analytical techniques, practices, and policies enforcement agencies are utilizing to determine whether a vertical merger poses potential competitive harm in violation of antitrust laws?

Parkinson: Enforcement authorities examine whether the merged entity would have the ability to foreclose rivals, the incentive to do so and the effect of foreclosure on competition overall. The merged company may have an ability to engage in input foreclosure if it has an important position upstream, such that downstream rivals might not be able to easily switch to other suppliers. For example, if there are few alternative suppliers, the alternative suppliers face capacity constraints or do not offer the same quality of product. Input foreclosure is more likely if the input is important to downstream rivals, either because it plays an important role in determining product quality or accounts for a substantial proportion of rivals’ costs. Engaging in input foreclosure can have costs as well as benefits for the merged company: it will lose sales upstream but may gain additional profits downstream. To understand whether the merged firm has an incentive to engage in input foreclosure, the agency will assess whether the benefits outweigh the costs, although this is often a complex area of economic analysis. Finally, if the merged company has the ability and incentive to engage in input foreclosure, the agency will assess whether that would harm competition. It may not do so, for example, if the merged company faces multiple rivals that are also vertically integrated.

Have you seen any recent updates to merger guidelines which will have an impact on vertical mergers going forward? To what extent do such guidelines reflect modern theoretical and empirical economic analysis?

Parkinson: The UK Competition and Markets Authority (CMA) issued new guidelines in 2021, replacing 2010 guidelines, with minimal changes to the analytical toolkit for assessing vertical mergers. However, the update may reflect a harder stance against some vertical mergers. The 2010 guidelines struck a relatively relaxed tone on vertical mergers, noting that most vertical mergers are benign and do not raise competition concerns. In contrast, the 2021 guidelines instead note that the UK authority has found competition concerns in several vertical mergers, and that commentators have warned of under-enforcement against vertical mergers. In addition, the 2021 guidelines are more skeptical of the efficiencies which can be generated by vertical mergers.

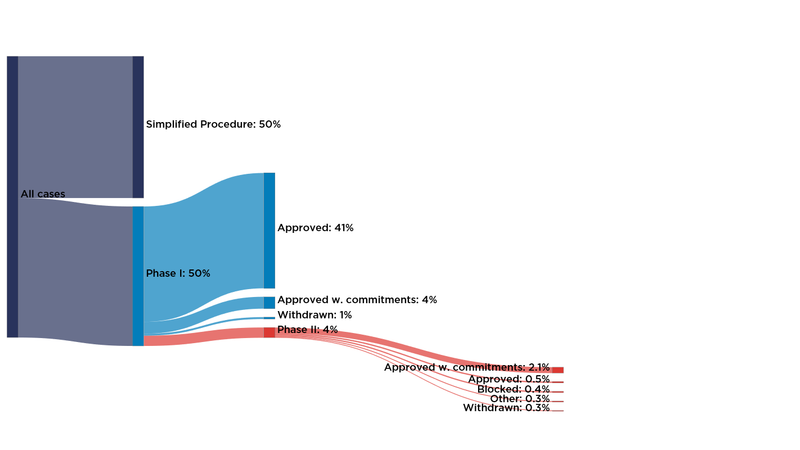

Could you highlight any recent cases which illustrate current antitrust enforcement efforts? What might we learn from their outcome?

Parkinson: In the UK, the CMA has assessed a number of vertical mergers in recent years. In Thermo Fisher and Roper, the authority assessed the acquisition of a supplier of peripherals for electron microscopes by a supplier of electron microscopes. The CMA found that, post-merger, Thermo Fisher would have the ability and incentive to engage in input foreclosure, stopping or degrading the supply of peripherals to rivals. Moreover, the CMA found that the long-term supply contracts in place would not sufficiently protect rivals. The transaction was ultimately abandoned. By contrast, the CMA unconditionally cleared the acquisition by BT – the UK’s largest fixed telecoms business – of EE, the UK’s largest mobile telecoms business. The merger raised multiple vertical issues, including BT’s supply of backhaul to mobile network operators. Despite a number of concerns expressed by other mobile network operators, the CMA concluded that, post-merger, BT would not have the ability and incentive to engage in input foreclosure. In contrast, the CMA found that some customers would be protected by their existing contracts. The differing outcomes in these cases illustrate that the assessment of vertical mergers is heavily fact-specific and relies on detailed economic analysis.

To what extent have courts applied different legal standards to vertical mergers? What difficulties does this pose for those companies pursuing vertical transactions?

Parkinson: The CMA has been particularly active in challenging vertical mergers, with a number of transactions abandoned or prohibited in recent years. This includes transactions that were not challenged by other authorities, such as Thermo Fisher and Roper, both US-based companies. Companies should be aware of divergences in approach between authorities worldwide when assessing potential vertical mergers.

Against the current regulatory and political backdrop, what advice would you offer to companies considering a vertical merger in the current market?

Parkinson: An assessment of antitrust risk is always important. It is often useful to involve economic advisers at an early stage if the risk assessment is not clear-cut. Economic analysis is particularly important and complex in vertical mergers and involving economic advisers will help in fully understanding the way in which the economists at the competition authorities will assess the vertical merger and therefore the associated risk to the transaction. Economic advisers can also help to start building a positive case for the transaction early in the process.

What trends do you expect to see in antitrust policy and enforcement over the months ahead? How is this likely to shape vertical merger activity levels going forward?

Parkinson: The trend appears to be toward closer examination of vertical mergers, and potentially increased enforcement. However, this may not necessarily reduce vertical merger activity levels, due to the attractiveness and potential benefits of vertical integration to many companies. Where one of the merging parties supplies an important input to rivals, the companies should prepare themselves for a potentially lengthy antitrust review.

Related

-

-

Article • 09 Apr 2021

Expert Opinion: Analyzing European Commission Merger Decisions

-

Article • 15 Jan 2021

How Will Merger Control Adapt to Recent Challenges?