UK Mergers: one year on from the “reset”

Share

Perceptions of the UK merger regime: one year on from the reset

At our 20th UK Competition Policy Forum, we met senior figures and experts in UK competition practice to discuss the state of the UK merger regime.

A year ago, the CMA’s “reset” was still fresh. The authority had promised to evolve its approach, guided by pace, predictability, proportionality, and process. It sought to bolster business confidence and growth, following the government’s call to “rip up the bureaucracy that blocks investment”. It also needed a new Chair. What that would mean in practice, however, was not yet clear.

Twelve months on, the tone from the CMA has shifted, but does that reflect a new approach or simply a new speech writer? Looking at both substance and perception, we discussed how far the merger regime has changed over the past year – in its process, its outcomes, and the CMA’s role as an independent and effective competition authority. Here are our reflections on the discussion.

These are reflections on a discussion conducted under Chatham House rules; they are not minutes of that discussion. The views expressed are the views of the authors only and do not necessarily represent the views of the UK Competition Policy Forum participants or Compass Lexecon, its management, its subsidiaries, its affiliates, its employees or its clients.

Reflecting on the merger investigation process since the reset

- A more open and transparent process during investigations. In the last year, the CMA has engaged early, particularly at senior levels. It has shown greater desire to identify the heart of the issue, for instance by drawing on ‘teach-ins’ more than before. Signals that it would be more open to the possibility of efficiencies and remedies have been matched by its actions. This change in the ‘user experience’ is significant; in stark contrast to a period when the degree of professional scepticism at the CMA had left even some of the parties whose transactions were cleared at Phase 2 feeling ‘treated like a criminal’.

- More, not less, transparency is needed after an investigation. Last year, we were concerned that, post-reset, the CMA would reduce the length of its written decisions and the detail they contain on its reasoning. It has. This lack of transparency matters, because clarity on the CMA’s considerations and evidence is crucial to a well-functioning and predictable system. The better parties can prepare, the less friction its process creates.

- The need for transparency is most acute where the CMA is evolving its approach. The CMA has been open about where it seeks to change, and consulted on how it should do so. That is welcome. But its written decisions will be the crucial window into how the CMA actually addresses these matters in practice – from efficiencies, dynamic effects, resilience, and failing firms, to how non-structural remedies may address its concerns. Transparency is equally crucial, if not more so, to perceptions of the regime. The CMA can counter more cynical interpretations of its decisions – from either direction – only by demonstrating how it has considered the relevant facts and principles in each case.

Reflecting on the significant outcomes of the merger regime since the reset

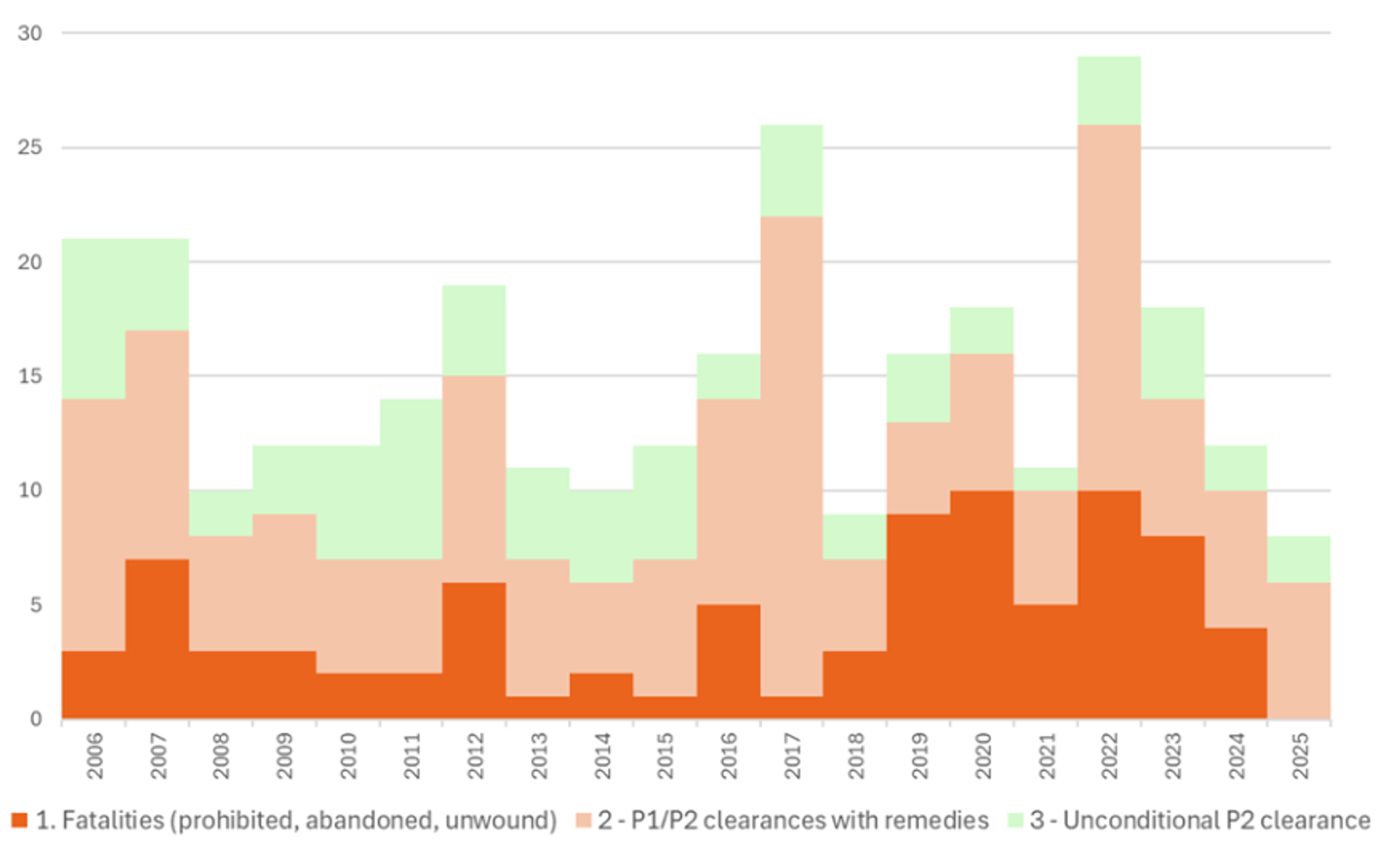

- An improving investigative process… that has too few investigations. The CMA made eight ‘significant’ interventions in 2025: six clearances with remedies, and two unconditional clearances at phase 2.[1] Broadly, each of these interventions was a reasonable process and a reasonable outcome. However, it was the lowest number of significant outcomes in 20 years. The reduction is not explained by exogenous factors, such as underlying merger activity; but rather appears to reflect a change in approach. Briefing papers that would likely have been called in before the reset no longer are. Potentially, that may represent some gain in efficiency. But the CMA must guard against under-enforcement, including the perception of under-enforcement. We shall see how this trend develops. So far, three months into 2026, there has been one fatality, a phase 2 clearance, and three significant interventions are currently pending.[2]

Figure 1: ‘Significant’ outcomes in UK merger control, by ultimate decision date |

|

Notes: (1) Data complete to 1 March 2026; (2) “Significant outcomes” defined as all cases excluding unconditional P1 clearances or cases that did not result in a phase 1 investigation; (3) Date variable based on ultimate decision date, or original Phase 2 decision when appealed; (4) outcomes where a transaction is blocked, unwound or abandoned on (presumed, unless otherwise known) antitrust grounds are classified as ‘fatalities’; (5) includes any ‘outsourcing’ by way of a UK Article 22 EUMR referral; (6) excludes bespoke water regulatory, NHS hospitals; and rail franchise cases. Source: Compass Lexecon analysis of CMA case data, using categorisation of “significant outcomes” and “fatalities” defined by Simon Pritchard and Benjamin Dubowitz in their paper “Brexit Parable” (forthcoming) |

- A less lethal regime. Sarah Cardell recently promised to reach for ‘a scalpel, not a sledgehammer’, highlighting the CMA’s greater willingness to use remedies to address its concerns, wherever possible. So far, that has been borne out in practice. Between 2018 and 2023, the UK merger regime was fatal for more than two in every five significant outcomes — counting all prohibitions, abandonments, and orders to unwind as ‘fatalities’. Between 2003 and 2017, fewer than one in every four significant outcomes were fatal. So far, the post-reset period is less lethal than either: only one merger has died since the start of 2025.

- As yet, no dramatic retreat from the world stage. Last year, we anticipated that the CMA would reduce the proportion of its investigations that focused on non-UK companies. Before 2018, one in nine of its investigations concerned only non-UK firms; after 2018, that proportion tripled to one in three. To some extent, the perceived impact that had on the UK’s attractiveness to foreign investment, appeared to have motivated the reset. So far, however, although the number of non-UK significant investigations has fallen, that is true for all investigations regardless of nationality. We will see whether that develops into a sustained trend.

Reflecting on the independence of the CMA since the reset

- An effective regulator cannot mark its own homework, or be perceived to do so. Errors happen. However, compared with the checks and balances in Europe and the US, the judicial review system provides limited scope for redress in the UK merger regime: a one-in-four chance of a ‘do-over’ with the same panel. To some extent, the panel system itself provided that check and balance (in principle, even if perhaps less so in practice). So, in removing it, the CMA must ensure that it does not erode the availability of effective recourse. Ensuring effective checks and balances against under-enforcement will be especially challenging. There is no clear and effective mechanism to challenge the CMA’s decision not to investigate.

- Competition policy does not exist in a vacuum: the independence and economic rationale of each decision will be under intense scrutiny. Government has a strategic role to play in competition policy, but not at the operational level. The CMA will need to actively demonstrate its operational independence and the clarity of its reasoning in each case. An effective regime cannot have, in fact or perception, a ‘black market’ of political interference.

- Competition policy is an enabler of growth, but that role must be applied with greater precision and principle if it is not to become self-defeating. In February, Sarah Cardell stated that ‘competition is not an objective in itself’. However, competition policy is not mere red tape. To avoid the perception of ‘growth washing’, the intellectual foundations of competition policy – set out in Aghion’s Nobel Prize winning work – must remain solid and conspicuous in the CMA’s decisions. Merger policy is an input, protecting the conditions for economic welfare and growth. A retreat to under-enforcement will tourniquet growth, rather than nourish it.

References

-

Synopsys / Ansys, Topps Tiles / CTD Tiles, Safran / Collins, GXO / Wincanton, SLB / ChampionX, and Greencore / Bakkavor were cleared with remedies. Global Business Travel / CWT and Boparan / ForFarmers (Burston and Radstock mills) were cleared at Phase 2 unconditionally. For the purpose of this analysis, we have allocated Spreadex / Sporting Index to 2024, the date of the original Phase 2 decision.

-

Aramark / Entier was ordered to unwind. Constellation Developments / Aston Barclay VR Holdings has been cleared unconditionally (subject to appeal). ABF / Hovis and Getty / Shutterstock are phase 2 investigations pending decisions at the time of writing. Vandemoortele / Délifrance will be referred for a phase 2 investigation unless the parties offer acceptable undertakings.